Note

Go to the end to download the full example code or to run this example in your browser via JupyterLite or Binder.

Post-tuning the decision threshold for cost-sensitive learning#

Once a classifier is trained, the output of the predict method outputs class label predictions corresponding to a thresholding of either the decision_function or the predict_proba output. For a binary classifier, the default threshold is defined as a posterior probability estimate of 0.5 or a decision score of 0.0.

However, this default strategy is most likely not optimal for the task at hand. Here, we use the “Statlog” German credit dataset [1] to illustrate a use case. In this dataset, the task is to predict whether a person has a “good” or “bad” credit. In addition, a cost-matrix is provided that specifies the cost of misclassification. Specifically, misclassifying a “bad” credit as “good” is five times more costly on average than misclassifying a “good” credit as “bad”.

We use the TunedThresholdClassifierCV to select the

cut-off point of the decision function that minimizes the provided business

cost.

In the second part of the example, we further extend this approach by considering the problem of fraud detection in credit card transactions: in this case, the business metric depends on the amount of each individual transaction.

References

# Authors: The scikit-learn developers

# SPDX-License-Identifier: BSD-3-Clause

Cost-sensitive learning with constant gains and costs#

In this first section, we illustrate the use of the

TunedThresholdClassifierCV in a setting of

cost-sensitive learning when the gains and costs associated to each entry of the

confusion matrix are constant. We use the problematic presented in [2] using the

“Statlog” German credit dataset [1].

“Statlog” German credit dataset#

We fetch the German credit dataset from OpenML.

import sklearn

from sklearn.datasets import fetch_openml

sklearn.set_config(transform_output="pandas")

german_credit = fetch_openml(data_id=31, as_frame=True, parser="pandas")

X, y = german_credit.data, german_credit.target

We check the feature types available in X.

X.info()

<class 'pandas.DataFrame'>

RangeIndex: 1000 entries, 0 to 999

Data columns (total 20 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 checking_status 1000 non-null category

1 duration 1000 non-null int64

2 credit_history 1000 non-null category

3 purpose 1000 non-null category

4 credit_amount 1000 non-null int64

5 savings_status 1000 non-null category

6 employment 1000 non-null category

7 installment_commitment 1000 non-null int64

8 personal_status 1000 non-null category

9 other_parties 1000 non-null category

10 residence_since 1000 non-null int64

11 property_magnitude 1000 non-null category

12 age 1000 non-null int64

13 other_payment_plans 1000 non-null category

14 housing 1000 non-null category

15 existing_credits 1000 non-null int64

16 job 1000 non-null category

17 num_dependents 1000 non-null int64

18 own_telephone 1000 non-null category

19 foreign_worker 1000 non-null category

dtypes: category(13), int64(7)

memory usage: 68.9 KB

Many features are categorical and usually string-encoded. We need to encode these categories when we develop our predictive model. Let’s check the targets.

y.value_counts()

class

good 700

bad 300

Name: count, dtype: int64

Another observation is that the dataset is imbalanced. We would need to be careful when evaluating our predictive model and use a family of metrics that are adapted to this setting.

In addition, we observe that the target is string-encoded. Some metrics (e.g. precision and recall) require to provide the label of interest also called the “positive label”. Here, we define that our goal is to predict whether or not a sample is a “bad” credit.

pos_label, neg_label = "bad", "good"

To carry our analysis, we split our dataset using a single stratified split.

from sklearn.model_selection import train_test_split

X_train, X_test, y_train, y_test = train_test_split(X, y, stratify=y, random_state=0)

We are ready to design our predictive model and the associated evaluation strategy.

Evaluation metrics#

In this section, we define a set of metrics that we use later. To see the effect of tuning the cut-off point, we evaluate the predictive model using the Receiver Operating Characteristic (ROC) curve and the Precision-Recall curve. The values reported on these plots are therefore the true positive rate (TPR), also known as the recall or the sensitivity, and the false positive rate (FPR), also known as the specificity, for the ROC curve and the precision and recall for the Precision-Recall curve.

From these four metrics, scikit-learn does not provide a scorer for the FPR. We therefore need to define a small custom function to compute it.

from sklearn.metrics import confusion_matrix

def fpr_score(y, y_pred, neg_label, pos_label):

cm = confusion_matrix(y, y_pred, labels=[neg_label, pos_label])

tn, fp, _, _ = cm.ravel()

tnr = tn / (tn + fp)

return 1 - tnr

As previously stated, the “positive label” is not defined as the value “1” and calling some of the metrics with this non-standard value raise an error. We need to provide the indication of the “positive label” to the metrics.

We therefore need to define a scikit-learn scorer using

make_scorer where the information is passed. We store all

the custom scorers in a dictionary. To use them, we need to pass the fitted model,

the data and the target on which we want to evaluate the predictive model.

from sklearn.metrics import make_scorer, precision_score, recall_score

tpr_score = recall_score # TPR and recall are the same metric

scoring = {

"precision": make_scorer(precision_score, pos_label=pos_label),

"recall": make_scorer(recall_score, pos_label=pos_label),

"fpr": make_scorer(fpr_score, neg_label=neg_label, pos_label=pos_label),

"tpr": make_scorer(tpr_score, pos_label=pos_label),

}

In addition, the original research [1] defines a custom business metric. We call a “business metric” any metric function that aims at quantifying how the predictions (correct or wrong) might impact the business value of deploying a given machine learning model in a specific application context. For our credit prediction task, the authors provide a custom cost-matrix which encodes that classifying a “bad” credit as “good” is 5 times more costly on average than the opposite: it is less costly for the financing institution to not grant a credit to a potential customer that will not default (and therefore miss a good customer that would have otherwise both reimbursed the credit and paid interests) than to grant a credit to a customer that will default.

We define a python function that weighs the confusion matrix and returns the overall cost. The rows of the confusion matrix hold the counts of observed classes while the columns hold counts of predicted classes. Recall that here we consider “bad” as the positive class (second row and column). Scikit-learn model selection tools expect that we follow a convention that “higher” means “better”, hence the following gain matrix assigns negative gains (costs) to the two kinds of prediction errors:

a gain of

-1for each false positive (“good” credit labeled as “bad”),a gain of

-5for each false negative (“bad” credit labeled as “good”),a

0gain for true positives and true negatives.

Note that theoretically, given that our model is calibrated and our data set representative and large enough, we do not need to tune the threshold, but can safely set it to 1/5 of the cost ratio, as stated by Eq. (2) in Elkan’s paper [2].

import numpy as np

def credit_gain_score(y, y_pred, neg_label, pos_label):

cm = confusion_matrix(y, y_pred, labels=[neg_label, pos_label])

gain_matrix = np.array(

[

[0, -1], # -1 gain for false positives

[-5, 0], # -5 gain for false negatives

]

)

return np.sum(cm * gain_matrix)

scoring["credit_gain"] = make_scorer(

credit_gain_score, neg_label=neg_label, pos_label=pos_label

)

Vanilla predictive model#

We use HistGradientBoostingClassifier as a predictive model

that natively handles categorical features and missing values.

from sklearn.ensemble import HistGradientBoostingClassifier

model = HistGradientBoostingClassifier(

categorical_features="from_dtype", random_state=0

).fit(X_train, y_train)

model

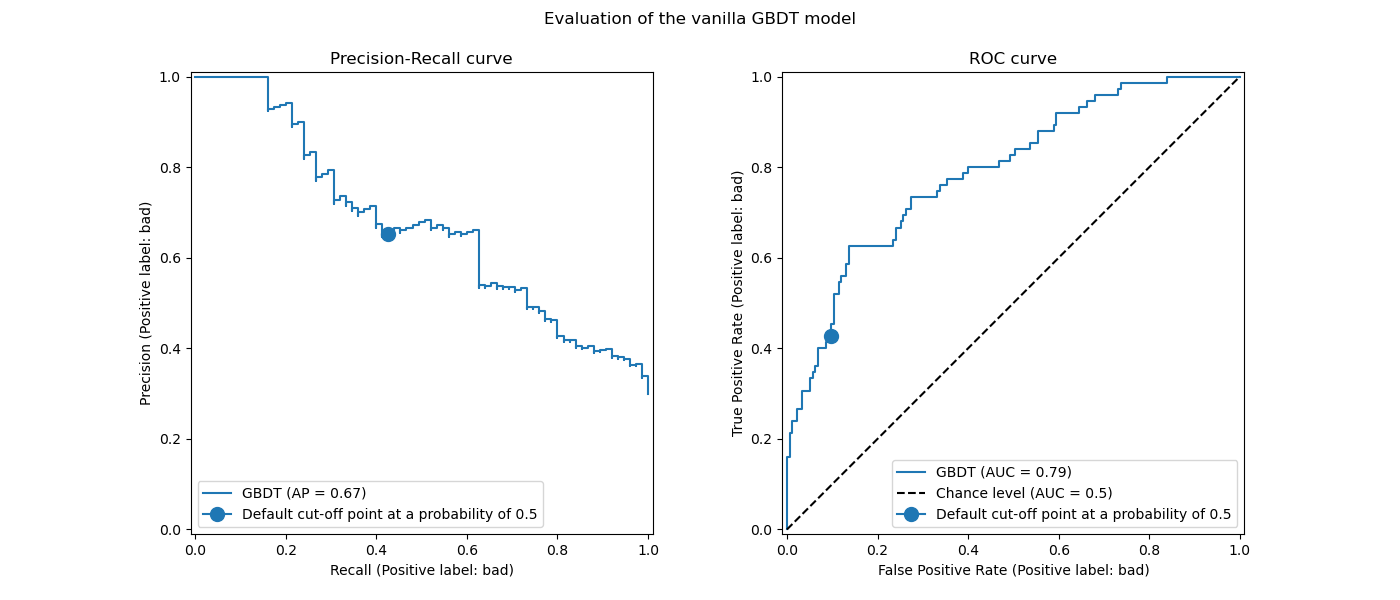

We evaluate the performance of our predictive model using the ROC and Precision-Recall curves.

import matplotlib.pyplot as plt

from sklearn.metrics import PrecisionRecallDisplay, RocCurveDisplay

fig, axs = plt.subplots(nrows=1, ncols=2, figsize=(14, 6))

PrecisionRecallDisplay.from_estimator(

model, X_test, y_test, pos_label=pos_label, ax=axs[0], name="GBDT"

)

axs[0].plot(

scoring["recall"](model, X_test, y_test),

scoring["precision"](model, X_test, y_test),

marker="o",

markersize=10,

color="tab:blue",

label="Default cut-off point at a probability of 0.5",

)

axs[0].set_title("Precision-Recall curve")

axs[0].legend()

RocCurveDisplay.from_estimator(

model,

X_test,

y_test,

pos_label=pos_label,

ax=axs[1],

name="GBDT",

plot_chance_level=True,

)

axs[1].plot(

scoring["fpr"](model, X_test, y_test),

scoring["tpr"](model, X_test, y_test),

marker="o",

markersize=10,

color="tab:blue",

label="Default cut-off point at a probability of 0.5",

)

axs[1].set_title("ROC curve")

axs[1].legend()

_ = fig.suptitle("Evaluation of the vanilla GBDT model")

We recall that these curves give insights on the statistical performance of the predictive model for different cut-off points. For the Precision-Recall curve, the reported metrics are the precision and recall and for the ROC curve, the reported metrics are the TPR (same as recall) and FPR.

Here, the different cut-off points correspond to different levels of posterior

probability estimates ranging between 0 and 1. By default, model.predict uses a

cut-off point at a probability estimate of 0.5. The metrics for such a cut-off point

are reported with the blue dot on the curves: it corresponds to the statistical

performance of the model when using model.predict.

However, we recall that the original aim was to minimize the cost (or maximize the gain) as defined by the business metric. We can compute the value of the business metric:

print(f"Business defined metric: {scoring['credit_gain'](model, X_test, y_test)}")

Business defined metric: -209

At this stage we don’t know if any other cut-off can lead to a greater gain. To find

the optimal one, we need to compute the cost-gain using the business metric for all

possible cut-off points and choose the best. This strategy can be quite tedious to

implement by hand, but the

TunedThresholdClassifierCV class is here to help us.

It automatically computes the cost-gain for all possible cut-off points and optimizes

for the scoring.

Tuning the cut-off point#

We use TunedThresholdClassifierCV to tune the

cut-off point. We need to provide the business metric to optimize as well as the

positive label. Internally, the optimum cut-off point is chosen such that it maximizes

the business metric via cross-validation. By default a 5-fold stratified

cross-validation is used.

from sklearn.model_selection import TunedThresholdClassifierCV

tuned_model = TunedThresholdClassifierCV(

estimator=model,

scoring=scoring["credit_gain"],

store_cv_results=True, # necessary to inspect all results

)

tuned_model.fit(X_train, y_train)

print(f"{tuned_model.best_threshold_=:0.2f}")

tuned_model.best_threshold_=0.03

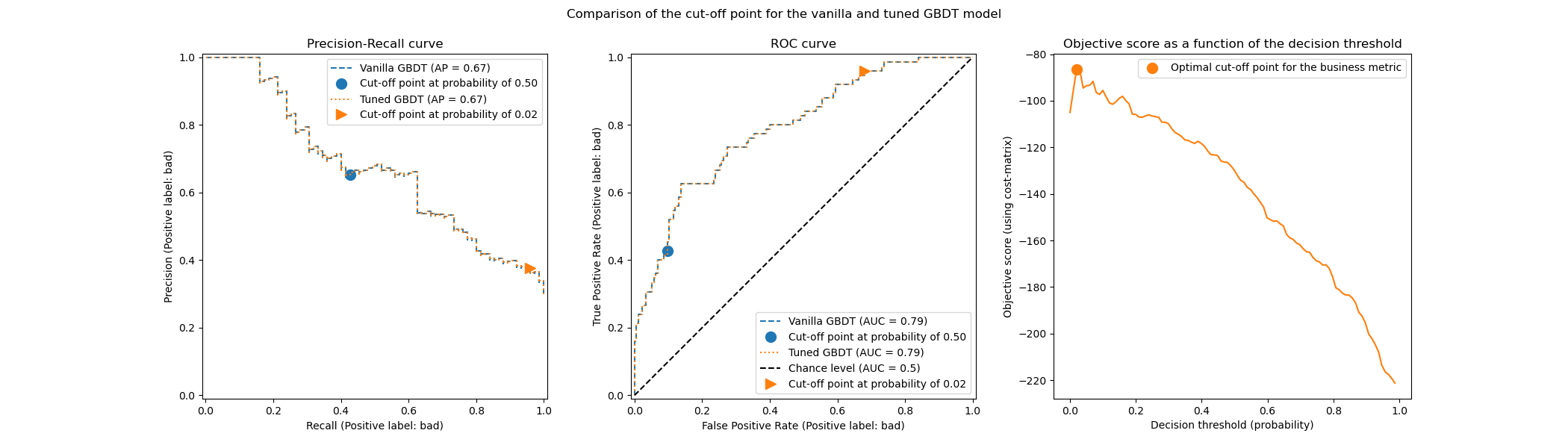

We plot the ROC and Precision-Recall curves for the vanilla model and the tuned model. Also we plot the cut-off points that would be used by each model. Because, we are reusing the same code later, we define a function that generates the plots.

def plot_roc_pr_curves(vanilla_model, tuned_model, *, title):

fig, axs = plt.subplots(nrows=1, ncols=3, figsize=(21, 6))

linestyles = ("dashed", "dotted")

markerstyles = ("o", ">")

colors = ("tab:blue", "tab:orange")

names = ("Vanilla GBDT", "Tuned GBDT")

for idx, (est, linestyle, marker, color, name) in enumerate(

zip((vanilla_model, tuned_model), linestyles, markerstyles, colors, names)

):

decision_threshold = getattr(est, "best_threshold_", 0.5)

PrecisionRecallDisplay.from_estimator(

est,

X_test,

y_test,

pos_label=pos_label,

ax=axs[0],

name=name,

curve_kwargs={"linestyle": linestyle, "color": color},

)

axs[0].plot(

scoring["recall"](est, X_test, y_test),

scoring["precision"](est, X_test, y_test),

marker,

markersize=10,

color=color,

label=f"Cut-off point at probability of {decision_threshold:.2f}",

)

RocCurveDisplay.from_estimator(

est,

X_test,

y_test,

pos_label=pos_label,

curve_kwargs={"linestyle": linestyle, "color": color},

ax=axs[1],

name=name,

plot_chance_level=idx == 1,

)

axs[1].plot(

scoring["fpr"](est, X_test, y_test),

scoring["tpr"](est, X_test, y_test),

marker,

markersize=10,

color=color,

label=f"Cut-off point at probability of {decision_threshold:.2f}",

)

axs[0].set_title("Precision-Recall curve")

axs[0].legend()

axs[1].set_title("ROC curve")

axs[1].legend()

axs[2].plot(

tuned_model.cv_results_["thresholds"],

tuned_model.cv_results_["scores"],

color="tab:orange",

)

axs[2].plot(

tuned_model.best_threshold_,

tuned_model.best_score_,

"o",

markersize=10,

color="tab:orange",

label="Optimal cut-off point for the business metric",

)

axs[2].legend()

axs[2].set_xlabel("Decision threshold (probability)")

axs[2].set_ylabel("Objective score (using cost-matrix)")

axs[2].set_title("Objective score as a function of the decision threshold")

fig.suptitle(title)

title = "Comparison of the cut-off point for the vanilla and tuned GBDT model"

plot_roc_pr_curves(model, tuned_model, title=title)

The first remark is that both classifiers have exactly the same ROC and Precision-Recall curves. It is expected because by default, the classifier is fitted on the same training data. In a later section, we discuss more in detail the available options regarding model refitting and cross-validation.

The second remark is that the cut-off points of the vanilla and tuned model are different. To understand why the tuned model has chosen this cut-off point, we can look at the right-hand side plot that plots the objective score that is our exactly the same as our business metric. We see that the optimum threshold corresponds to the maximum of the objective score. This maximum is reached for a decision threshold much lower than 0.5: the tuned model enjoys a much higher recall at the cost of of significantly lower precision: the tuned model is much more eager to predict the “bad” class label to larger fraction of individuals.

We can now check if choosing this cut-off point leads to a better score on the testing set:

print(f"Business defined metric: {scoring['credit_gain'](tuned_model, X_test, y_test)}")

Business defined metric: -143

We observe that tuning the decision threshold almost improves our business gains by factor of 2.

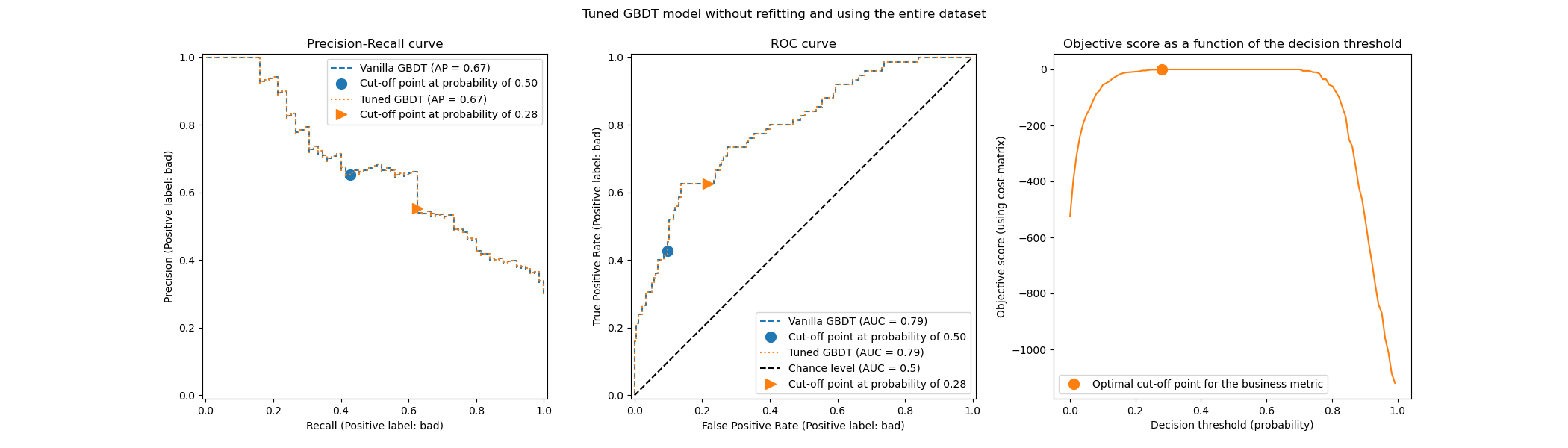

Consideration regarding model refitting and cross-validation#

In the above experiment, we used the default setting of the

TunedThresholdClassifierCV. In particular, the

cut-off point is tuned using a 5-fold stratified cross-validation. Also, the

underlying predictive model is refitted on the entire training data once the cut-off

point is chosen.

These two strategies can be changed by providing the refit and cv parameters.

For instance, one could provide a fitted estimator and set cv="prefit", in which

case the cut-off point is found on the entire dataset provided at fitting time.

Also, the underlying classifier is not be refitted by setting refit=False. Here, we

can try to do such experiment.

model.fit(X_train, y_train)

tuned_model.set_params(cv="prefit", refit=False).fit(X_train, y_train)

print(f"{tuned_model.best_threshold_=:0.2f}")

tuned_model.best_threshold_=0.25

Then, we evaluate our model with the same approach as before:

title = "Tuned GBDT model without refitting and using the entire dataset"

plot_roc_pr_curves(model, tuned_model, title=title)

We observe the that the optimum cut-off point is different from the one found in the previous experiment. If we look at the right-hand side plot, we observe that the business gain has large plateau of near-optimal 0 gain for a large span of decision thresholds. This behavior is symptomatic of an overfitting. Because we disable cross-validation, we tuned the cut-off point on the same set as the model was trained on, and this is the reason for the observed overfitting.

This option should therefore be used with caution. One needs to make sure that the

data provided at fitting time to the

TunedThresholdClassifierCV is not the same as the

data used to train the underlying classifier. This could happen sometimes when the

idea is just to tune the predictive model on a completely new validation set without a

costly complete refit.

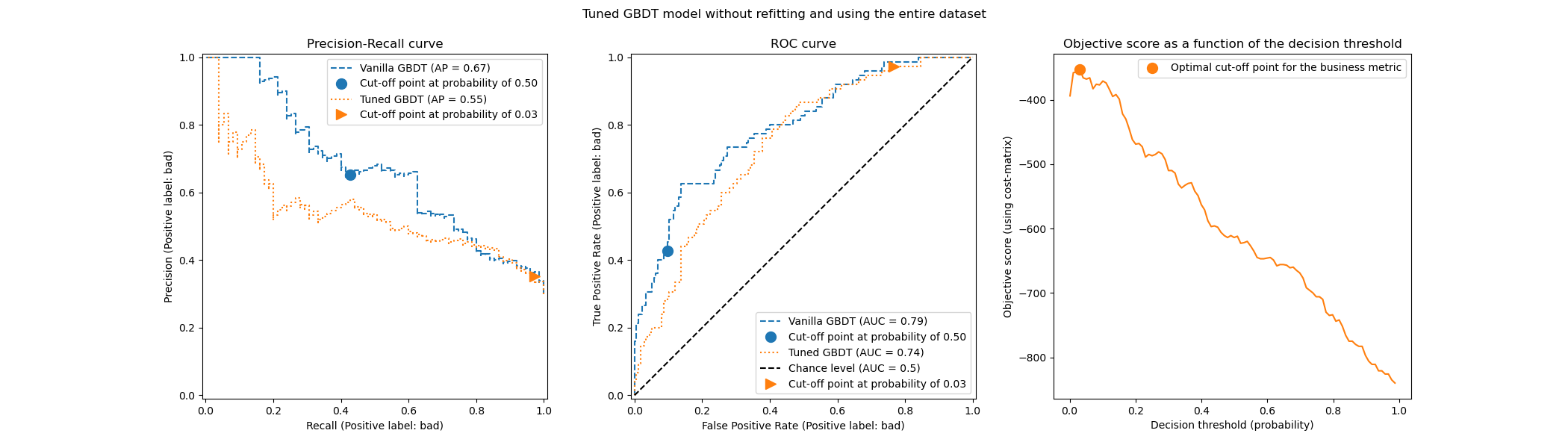

When cross-validation is too costly, a potential alternative is to use a

single train-test split by providing a floating number in range [0, 1] to the cv

parameter. It splits the data into a training and testing set. Let’s explore this

option:

tuned_model.set_params(cv=0.75).fit(X_train, y_train)

title = "Tuned GBDT model without refitting and using the entire dataset"

plot_roc_pr_curves(model, tuned_model, title=title)

Regarding the cut-off point, we observe that the optimum is similar to the multiple repeated cross-validation case. However, be aware that a single split does not account for the variability of the fit/predict process and thus we are unable to know if there is any variance in the cut-off point. The repeated cross-validation averages out this effect.

Another observation concerns the ROC and Precision-Recall curves of the tuned model. As expected, these curves differ from those of the vanilla model, given that we trained the underlying classifier on a subset of the data provided during fitting and reserved a validation set for tuning the cut-off point.

Cost-sensitive learning when gains and costs are not constant#

As stated in [2], gains and costs are generally not constant in real-world problems. In this section, we use a similar example as in [2] for the problem of detecting fraud in credit card transaction records.

The credit card dataset#

credit_card = fetch_openml(data_id=1597, as_frame=True, parser="pandas")

credit_card.frame.info()

<class 'pandas.DataFrame'>

RangeIndex: 284807 entries, 0 to 284806

Data columns (total 30 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 V1 284807 non-null float64

1 V2 284807 non-null float64

2 V3 284807 non-null float64

3 V4 284807 non-null float64

4 V5 284807 non-null float64

5 V6 284807 non-null float64

6 V7 284807 non-null float64

7 V8 284807 non-null float64

8 V9 284807 non-null float64

9 V10 284807 non-null float64

10 V11 284807 non-null float64

11 V12 284807 non-null float64

12 V13 284807 non-null float64

13 V14 284807 non-null float64

14 V15 284807 non-null float64

15 V16 284807 non-null float64

16 V17 284807 non-null float64

17 V18 284807 non-null float64

18 V19 284807 non-null float64

19 V20 284807 non-null float64

20 V21 284807 non-null float64

21 V22 284807 non-null float64

22 V23 284807 non-null float64

23 V24 284807 non-null float64

24 V25 284807 non-null float64

25 V26 284807 non-null float64

26 V27 284807 non-null float64

27 V28 284807 non-null float64

28 Amount 284807 non-null float64

29 Class 284807 non-null category

dtypes: category(1), float64(29)

memory usage: 63.3 MB

The dataset contains information about credit card records from which some are fraudulent and others are legitimate. The goal is therefore to predict whether or not a credit card record is fraudulent.

columns_to_drop = ["Class"]

data = credit_card.frame.drop(columns=columns_to_drop)

target = credit_card.frame["Class"].astype(int)

First, we check the class distribution of the datasets.

target.value_counts(normalize=True)

Class

0 0.998273

1 0.001727

Name: proportion, dtype: float64

The dataset is highly imbalanced with fraudulent transaction representing only 0.17% of the data. Since we are interested in training a machine learning model, we should also make sure that we have enough samples in the minority class to train the model.

target.value_counts()

Class

0 284315

1 492

Name: count, dtype: int64

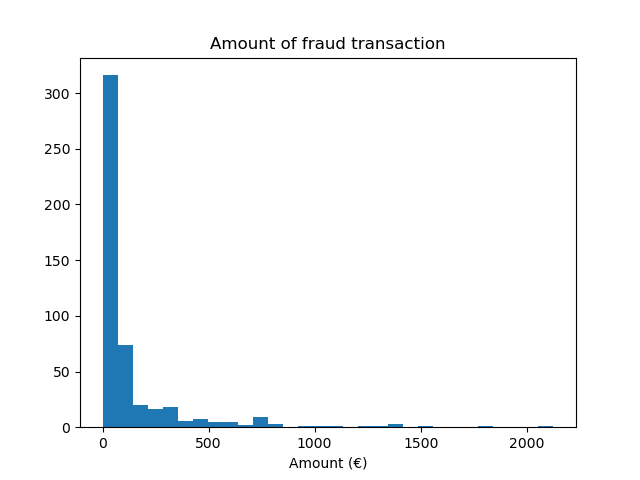

We observe that we have around 500 samples that is on the low end of the number of samples required to train a machine learning model. In addition of the target distribution, we check the distribution of the amount of the fraudulent transactions.

fraud = target == 1

amount_fraud = data["Amount"][fraud]

_, ax = plt.subplots()

ax.hist(amount_fraud, bins=30)

ax.set_title("Amount of fraud transaction")

_ = ax.set_xlabel("Amount (€)")

Addressing the problem with a business metric#

Now, we create the business metric that depends on the amount of each transaction. We define the cost matrix similarly to [2]. Accepting a legitimate transaction provides a gain of 2% of the amount of the transaction. However, accepting a fraudulent transaction result in a loss of the amount of the transaction. As stated in [2], the gain and loss related to refusals (of fraudulent and legitimate transactions) are not trivial to define. Here, we define that a refusal of a legitimate transaction is estimated to a loss of 5€ while the refusal of a fraudulent transaction is estimated to a gain of 50€. Therefore, we define the following function to compute the total benefit of a given decision:

def business_metric(y_true, y_pred, amount):

mask_true_positive = (y_true == 1) & (y_pred == 1)

mask_true_negative = (y_true == 0) & (y_pred == 0)

mask_false_positive = (y_true == 0) & (y_pred == 1)

mask_false_negative = (y_true == 1) & (y_pred == 0)

fraudulent_refuse = mask_true_positive.sum() * 50

fraudulent_accept = -amount[mask_false_negative].sum()

legitimate_refuse = mask_false_positive.sum() * -5

legitimate_accept = (amount[mask_true_negative] * 0.02).sum()

return fraudulent_refuse + fraudulent_accept + legitimate_refuse + legitimate_accept

From this business metric, we create a scikit-learn scorer that given a fitted

classifier and a test set compute the business metric. In this regard, we use

the make_scorer factory. The variable amount is an

additional metadata to be passed to the scorer and we need to use

metadata routing to take into account this information.

sklearn.set_config(enable_metadata_routing=True)

business_scorer = make_scorer(business_metric).set_score_request(amount=True)

So at this stage, we observe that the amount of the transaction is used twice: once

as a feature to train our predictive model and once as a metadata to compute the

the business metric and thus the statistical performance of our model. When used as a

feature, we are only required to have a column in data that contains the amount of

each transaction. To use this information as metadata, we need to have an external

variable that we can pass to the scorer or the model that internally routes this

metadata to the scorer. So let’s create this variable.

amount = credit_card.frame["Amount"].to_numpy()

from sklearn.model_selection import train_test_split

data_train, data_test, target_train, target_test, amount_train, amount_test = (

train_test_split(

data, target, amount, stratify=target, test_size=0.5, random_state=42

)

)

We first evaluate some baseline policies to serve as reference. Recall that class “0” is the legitimate class and class “1” is the fraudulent class.

from sklearn.dummy import DummyClassifier

always_accept_policy = DummyClassifier(strategy="constant", constant=0)

always_accept_policy.fit(data_train, target_train)

benefit = business_scorer(

always_accept_policy, data_test, target_test, amount=amount_test

)

print(f"Benefit of the 'always accept' policy: {benefit:,.2f}€")

Benefit of the 'always accept' policy: 221,445.07€

A policy that considers all transactions as legitimate would create a profit of around 220,000€. We make the same evaluation for a classifier that predicts all transactions as fraudulent.

always_reject_policy = DummyClassifier(strategy="constant", constant=1)

always_reject_policy.fit(data_train, target_train)

benefit = business_scorer(

always_reject_policy, data_test, target_test, amount=amount_test

)

print(f"Benefit of the 'always reject' policy: {benefit:,.2f}€")

Benefit of the 'always reject' policy: -698,490.00€

Such a policy would entail a catastrophic loss: around 670,000€. This is expected since the vast majority of the transactions are legitimate and the policy would refuse them at a non-trivial cost.

A predictive model that adapts the accept/reject decisions on a per transaction basis should ideally allow us to make a profit larger than the 220,000€ of the best of our constant baseline policies.

We start with a logistic regression model with the default decision threshold

at 0.5. Here we tune the hyperparameter C of the logistic regression with a

proper scoring rule (the log loss) to ensure that the model’s probabilistic

predictions returned by its predict_proba method are as accurate as

possible, irrespectively of the choice of the value of the decision

threshold.

from sklearn.linear_model import LogisticRegression

from sklearn.model_selection import GridSearchCV

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import StandardScaler

logistic_regression = make_pipeline(StandardScaler(), LogisticRegression())

param_grid = {"logisticregression__C": np.logspace(-6, 6, 13)}

model = GridSearchCV(logistic_regression, param_grid, scoring="neg_log_loss").fit(

data_train, target_train

)

model

print(

"Benefit of logistic regression with default threshold: "

f"{business_scorer(model, data_test, target_test, amount=amount_test):,.2f}€"

)

Benefit of logistic regression with default threshold: 244,919.87€

The business metric shows that our predictive model with a default decision threshold is already winning over the baseline in terms of profit and it would be already beneficial to use it to accept or reject transactions instead of accepting all transactions.

Tuning the decision threshold#

Now the question is: is our model optimum for the type of decision that we want to do?

Up to now, we did not optimize the decision threshold. We use the

TunedThresholdClassifierCV to optimize the decision

given our business scorer. To avoid a nested cross-validation, we will use the

best estimator found during the previous grid-search.

tuned_model = TunedThresholdClassifierCV(

estimator=model.best_estimator_,

scoring=business_scorer,

thresholds=100,

n_jobs=2,

)

Since our business scorer requires the amount of each transaction, we need to pass

this information in the fit method. The

TunedThresholdClassifierCV is in charge of

automatically dispatching this metadata to the underlying scorer.

tuned_model.fit(data_train, target_train, amount=amount_train)

We observe that the tuned decision threshold is far away from the default 0.5:

print(f"Tuned decision threshold: {tuned_model.best_threshold_:.2f}")

Tuned decision threshold: 0.03

print(

"Benefit of logistic regression with a tuned threshold: "

f"{business_scorer(tuned_model, data_test, target_test, amount=amount_test):,.2f}€"

)

Benefit of logistic regression with a tuned threshold: 249,433.39€

We observe that tuning the decision threshold increases the expected profit when deploying our model - as indicated by the business metric. It is therefore valuable, whenever possible, to optimize the decision threshold with respect to the business metric.

Manually setting the decision threshold instead of tuning it#

In the previous example, we used the

TunedThresholdClassifierCV to find the optimal

decision threshold. However, in some cases, we might have some prior knowledge about

the problem at hand and we might be happy to set the decision threshold manually.

The class FixedThresholdClassifier allows us to

manually set the decision threshold. At prediction time, it behave as the previous

tuned model but no search is performed during the fitting process. Note that here

we use FrozenEstimator to wrap the predictive model to

avoid any refitting.

Here, we will reuse the decision threshold found in the previous section to create a new model and check that it gives the same results.

from sklearn.frozen import FrozenEstimator

from sklearn.model_selection import FixedThresholdClassifier

model_fixed_threshold = FixedThresholdClassifier(

estimator=FrozenEstimator(model), threshold=tuned_model.best_threshold_

)

business_score = business_scorer(

model_fixed_threshold, data_test, target_test, amount=amount_test

)

print(f"Benefit of logistic regression with a tuned threshold: {business_score:,.2f}€")

Benefit of logistic regression with a tuned threshold: 249,433.39€

We observe that we obtained the exact same results but the fitting process was much faster since we did not perform any hyper-parameter search.

Finally, the estimate of the (average) business metric itself can be unreliable, in particular when the number of data points in the minority class is very small. Any business impact estimated by cross-validation of a business metric on historical data (offline evaluation) should ideally be confirmed by A/B testing on live data (online evaluation). Note however that A/B testing models is beyond the scope of the scikit-learn library itself.

At the end, we disable the configuration flag for metadata routing:

.. GENERATED FROM PYTHON SOURCE LINES 693-694

sklearn.set_config(enable_metadata_routing=False)

Total running time of the script: (0 minutes 24.805 seconds)

Related examples

Post-hoc tuning the cut-off point of decision function

Custom refit strategy of a grid search with cross-validation