Note

Go to the end to download the full example code or to run this example in your browser via JupyterLite or Binder.

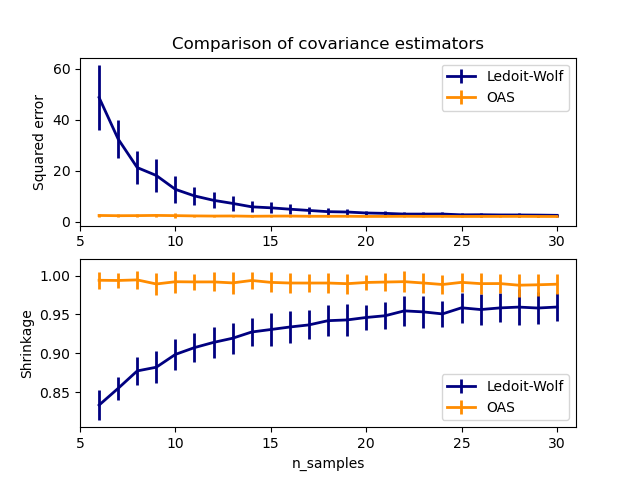

Ledoit-Wolf vs OAS estimation#

The usual covariance maximum likelihood estimate can be regularized using shrinkage. Ledoit and Wolf proposed a close formula to compute the asymptotically optimal shrinkage parameter (minimizing an MSE criterion), yielding the Ledoit-Wolf covariance estimate.

Chen et al. [1] proposed an improvement of the Ledoit-Wolf shrinkage parameter, the OAS coefficient, whose convergence is significantly better under the assumption that the data are Gaussian.

This example, inspired from Chen’s publication [1], shows a comparison of the estimated MSE of the LW and OAS methods, using Gaussian distributed data.

References

# Authors: The scikit-learn developers

# SPDX-License-Identifier: BSD-3-Clause

import matplotlib.pyplot as plt

import numpy as np

from scipy.linalg import cholesky, toeplitz

from sklearn.covariance import OAS, LedoitWolf

np.random.seed(0)

n_features = 100

# simulation covariance matrix (AR(1) process)

r = 0.1

real_cov = toeplitz(r ** np.arange(n_features))

coloring_matrix = cholesky(real_cov)

n_samples_range = np.arange(6, 31, 1)

repeat = 100

lw_mse = np.zeros((n_samples_range.size, repeat))

oa_mse = np.zeros((n_samples_range.size, repeat))

lw_shrinkage = np.zeros((n_samples_range.size, repeat))

oa_shrinkage = np.zeros((n_samples_range.size, repeat))

for i, n_samples in enumerate(n_samples_range):

for j in range(repeat):

X = np.dot(np.random.normal(size=(n_samples, n_features)), coloring_matrix.T)

lw = LedoitWolf(store_precision=False, assume_centered=True)

lw.fit(X)

lw_mse[i, j] = lw.error_norm(real_cov, scaling=False)

lw_shrinkage[i, j] = lw.shrinkage_

oa = OAS(store_precision=False, assume_centered=True)

oa.fit(X)

oa_mse[i, j] = oa.error_norm(real_cov, scaling=False)

oa_shrinkage[i, j] = oa.shrinkage_

# plot MSE

plt.subplot(2, 1, 1)

plt.errorbar(

n_samples_range,

lw_mse.mean(1),

yerr=lw_mse.std(1),

label="Ledoit-Wolf",

color="navy",

lw=2,

)

plt.errorbar(

n_samples_range,

oa_mse.mean(1),

yerr=oa_mse.std(1),

label="OAS",

color="darkorange",

lw=2,

)

plt.ylabel("Squared error")

plt.legend(loc="upper right")

plt.title("Comparison of covariance estimators")

plt.xlim(5, 31)

# plot shrinkage coefficient

plt.subplot(2, 1, 2)

plt.errorbar(

n_samples_range,

lw_shrinkage.mean(1),

yerr=lw_shrinkage.std(1),

label="Ledoit-Wolf",

color="navy",

lw=2,

)

plt.errorbar(

n_samples_range,

oa_shrinkage.mean(1),

yerr=oa_shrinkage.std(1),

label="OAS",

color="darkorange",

lw=2,

)

plt.xlabel("n_samples")

plt.ylabel("Shrinkage")

plt.legend(loc="lower right")

plt.ylim(plt.ylim()[0], 1.0 + (plt.ylim()[1] - plt.ylim()[0]) / 10.0)

plt.xlim(5, 31)

plt.show()

Total running time of the script: (0 minutes 3.655 seconds)

Related examples

Shrinkage covariance estimation: LedoitWolf vs OAS and max-likelihood

Normal, Ledoit-Wolf and OAS Linear Discriminant Analysis for classification