empirical_covariance#

- sklearn.covariance.empirical_covariance(X, *, assume_centered=False)[source]#

Compute the Maximum likelihood covariance estimator.

- Parameters:

- Xndarray of shape (n_samples, n_features)

Data from which to compute the covariance estimate.

- assume_centeredbool, default=False

If

True, data will not be centered before computation. Useful when working with data whose mean is almost, but not exactly zero. IfFalse, data will be centered before computation.

- Returns:

- covariancendarray of shape (n_features, n_features)

Empirical covariance (Maximum Likelihood Estimator).

Examples

>>> from sklearn.covariance import empirical_covariance >>> X = [[1,1,1],[1,1,1],[1,1,1], ... [0,0,0],[0,0,0],[0,0,0]] >>> empirical_covariance(X) array([[0.25, 0.25, 0.25], [0.25, 0.25, 0.25], [0.25, 0.25, 0.25]])

Gallery examples#

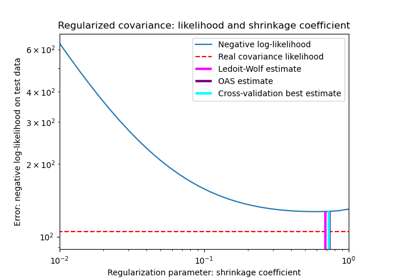

Shrinkage covariance estimation: LedoitWolf vs OAS and max-likelihood

Shrinkage covariance estimation: LedoitWolf vs OAS and max-likelihood