1.1. Linear Models#

The following are a set of methods intended for regression in which the target value is expected to be a linear combination of the features. In mathematical notation, the predicted value \(\hat{y}\) can be written as:

Across the module, we designate the vector \(w = (w_1,

..., w_p)\) as coef_ and \(w_0\) as intercept_.

To perform classification with generalized linear models, see Logistic regression.

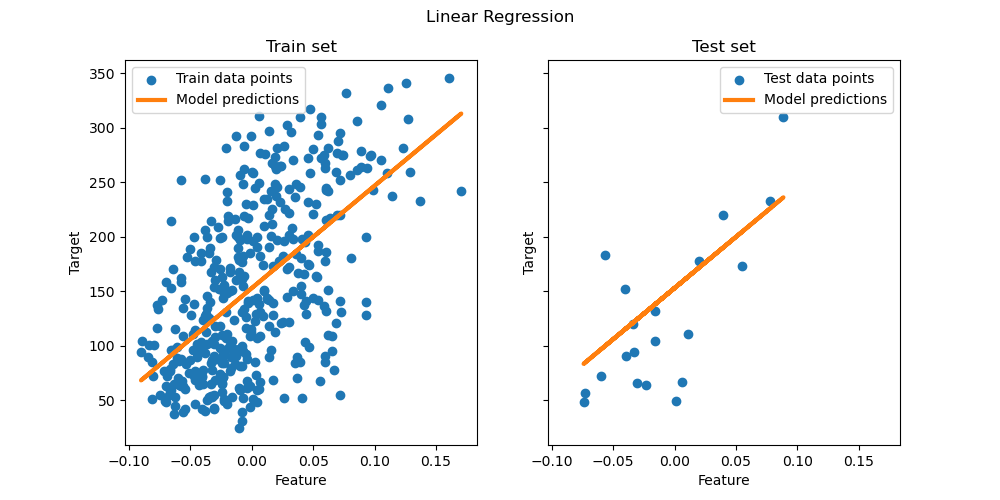

1.1.1. Ordinary Least Squares#

LinearRegression fits a linear model with coefficients

\(w = (w_1, ..., w_p)\) to minimize the residual sum

of squares between the observed targets in the dataset, and the

targets predicted by the linear approximation. Mathematically it

solves a problem of the form:

LinearRegression takes in its fit method arguments X, y,

sample_weight and stores the coefficients \(w\) of the linear model in its

coef_ and intercept_ attributes:

>>> from sklearn import linear_model

>>> reg = linear_model.LinearRegression()

>>> reg.fit([[0, 0], [1, 1], [2, 2]], [0, 1, 2])

LinearRegression()

>>> reg.coef_

array([0.5, 0.5])

>>> reg.intercept_

0.0

The coefficient estimates for Ordinary Least Squares rely on the independence of the features. When features are correlated and some columns of the design matrix \(X\) have an approximately linear dependence, the design matrix becomes close to singular and as a result, the least-squares estimate becomes highly sensitive to random errors in the observed target, producing a large variance. This situation of multicollinearity can arise, for example, when data are collected without an experimental design.

Examples

1.1.1.1. Non-Negative Least Squares#

It is possible to constrain all the coefficients to be non-negative, which may

be useful when they represent some physical or naturally non-negative

quantities (e.g., frequency counts or prices of goods).

LinearRegression accepts a boolean positive

parameter: when set to True Non-Negative Least Squares are then applied.

Examples

1.1.1.2. Ordinary Least Squares Complexity#

The least squares solution is computed using the singular value

decomposition of \(X\). If \(X\) is a matrix of shape (n_samples, n_features)

this method has a cost of

\(O(n_{\text{samples}} n_{\text{features}}^2)\), assuming that

\(n_{\text{samples}} \geq n_{\text{features}}\).

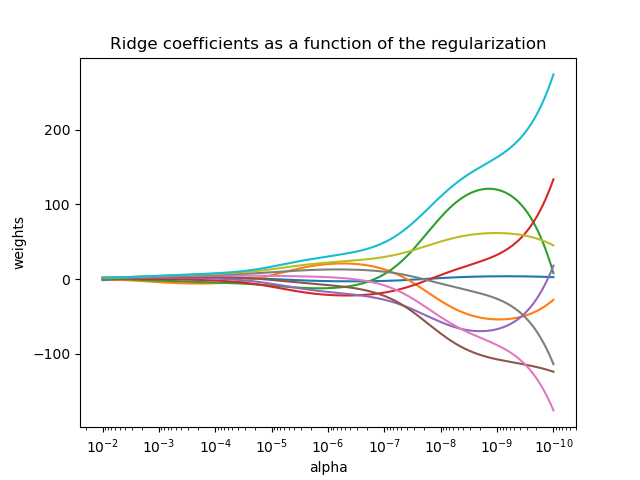

1.1.2. Ridge regression and classification#

1.1.2.1. Regression#

Ridge regression addresses some of the problems of

Ordinary Least Squares by imposing a penalty on the size of the

coefficients. The ridge coefficients minimize a penalized residual sum

of squares:

The complexity parameter \(\alpha \geq 0\) controls the amount of shrinkage: the larger the value of \(\alpha\), the greater the amount of shrinkage and thus the coefficients become more robust to collinearity.

As with other linear models, Ridge will take in its fit method

arrays X, y and will store the coefficients \(w\) of the linear model in

its coef_ member:

>>> from sklearn import linear_model

>>> reg = linear_model.Ridge(alpha=.5)

>>> reg.fit([[0, 0], [0, 0], [1, 1]], [0, .1, 1])

Ridge(alpha=0.5)

>>> reg.coef_

array([0.34545455, 0.34545455])

>>> reg.intercept_

np.float64(0.13636)

Note that the class Ridge allows for the user to specify that the

solver be automatically chosen by setting solver="auto". When this option

is specified, Ridge will choose between the "lbfgs", "cholesky",

and "sparse_cg" solvers. Ridge will begin checking the conditions

shown in the following table from top to bottom. If the condition is true,

the corresponding solver is chosen.

Solver |

Condition |

‘lbfgs’ |

The |

‘cholesky’ |

The input array X is not sparse. |

‘sparse_cg’ |

None of the above conditions are fulfilled. |

Examples

1.1.2.2. Classification#

The Ridge regressor has a classifier variant:

RidgeClassifier. This classifier first converts binary targets to

{-1, 1} and then treats the problem as a regression task, optimizing the

same objective as above. The predicted class corresponds to the sign of the

regressor’s prediction. For multiclass classification, the problem is

treated as multi-output regression, and the predicted class corresponds to

the output with the highest value.

It might seem questionable to use a (penalized) Least Squares loss to fit a

classification model instead of the more traditional logistic or hinge

losses. However, in practice, all those models can lead to similar

cross-validation scores in terms of accuracy or precision/recall, while the

penalized least squares loss used by the RidgeClassifier allows for

a very different choice of the numerical solvers with distinct computational

performance profiles.

The RidgeClassifier can be significantly faster than e.g.

LogisticRegression with a high number of classes because it can

compute the projection matrix \((X^T X)^{-1} X^T\) only once.

This classifier is sometimes referred to as a Least Squares Support Vector Machine with a linear kernel.

Examples

1.1.2.3. Ridge Complexity#

This method has the same order of complexity as Ordinary Least Squares.

1.1.2.4. Setting the regularization parameter: leave-one-out Cross-Validation#

RidgeCV and RidgeClassifierCV implement ridge

regression/classification with built-in cross-validation of the alpha parameter.

They work in the same way as GridSearchCV except

that it defaults to efficient Leave-One-Out cross-validation.

When using the default cross-validation, alpha cannot be 0 due to the

formulation used to calculate Leave-One-Out error. See [RL2007] for details.

Usage example:

>>> import numpy as np

>>> from sklearn import linear_model

>>> reg = linear_model.RidgeCV(alphas=np.logspace(-6, 6, 13))

>>> reg.fit([[0, 0], [0, 0.1], [1, 1]], [0, -0.1, 1])

RidgeCV(alphas=array([1.e-06, 1.e-05, 1.e-04, 1.e-03, 1.e-02, 1.e-01, 1.e+00, 1.e+01,

1.e+02, 1.e+03, 1.e+04, 1.e+05, 1.e+06]))

>>> reg.alpha_

np.float64(0.1)

Specifying the value of the cv attribute will trigger the use of

cross-validation with GridSearchCV, for

example cv=10 for 10-fold cross-validation, rather than Leave-One-Out

Cross-Validation.

References#

“Notes on Regularized Least Squares”, Rifkin & Lippert (technical report, course slides).

1.1.3. Lasso#

The Lasso is a linear model that estimates sparse coefficients, i.e., it is

able to set coefficients exactly to zero.

It is useful in some contexts due to its tendency to prefer solutions

with fewer non-zero coefficients, effectively reducing the number of

features upon which the given solution is dependent. For this reason,

Lasso and its variants are fundamental to the field of compressed sensing.

Under certain conditions, it can recover the exact set of non-zero coefficients (see

Compressive sensing: tomography reconstruction with L1 prior (Lasso)).

Mathematically, it consists of a linear model with an added regularization term. The objective function to minimize is:

The lasso estimate thus solves the least-squares with added penalty \(\alpha ||w||_1\), where \(\alpha\) is a constant and \(||w||_1\) is the \(\ell_1\)-norm of the coefficient vector.

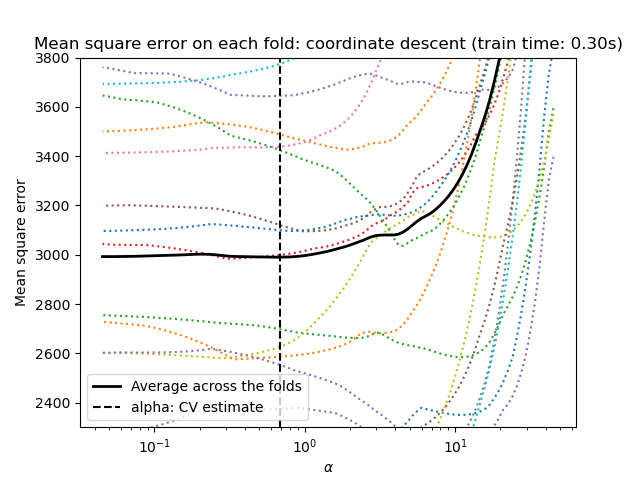

The implementation in the class Lasso uses coordinate descent as

the algorithm to fit the coefficients. See Least Angle Regression

for another implementation:

>>> from sklearn import linear_model

>>> reg = linear_model.Lasso(alpha=0.1)

>>> reg.fit([[0, 0], [1, 1]], [0, 1])

Lasso(alpha=0.1)

>>> reg.predict([[1, 1]])

array([0.8])

The function lasso_path is useful for lower-level tasks, as it

computes the coefficients along the full path of possible values.

Examples

Compressive sensing: tomography reconstruction with L1 prior (Lasso)

Common pitfalls in the interpretation of coefficients of linear models

Note

Feature selection with Lasso

As the Lasso regression yields sparse models, it can thus be used to perform feature selection, as detailed in L1-based feature selection.

References#

The following references explain the origin of the Lasso as well as properties of the Lasso problem and the duality gap computation used for convergence control.

“An Interior-Point Method for Large-Scale L1-Regularized Least Squares,” S. J. Kim, K. Koh, M. Lustig, S. Boyd and D. Gorinevsky, in IEEE Journal of Selected Topics in Signal Processing, 2007 (Paper)

1.1.3.1. Coordinate Descent with Gap Safe Screening Rules#

Coordinate descent (CD) is a strategy to solve a minimization problem that considers a single feature \(j\) at a time. This way, the optimization problem is reduced to a 1-dimensional problem which is easier to solve:

with index \(-j\) meaning all features but \(j\). The solution is

with the soft-thresholding function

\(S(z, \alpha) = \operatorname{sign}(z) \max(0, |z|-\alpha)\).

Note that the soft-thresholding function is exactly zero whenever

\(\alpha \geq |z|\).

The CD solver then loops over the features either in a cycle, picking one feature after

the other in the order given by X (selection="cyclic"), or by randomly picking

features (selection="random").

It stops if the duality gap is smaller than the provided tolerance tol.

Mathematical details#

The duality gap \(G(w, v)\) is an upper bound of the difference between the current primal objective function of the Lasso, \(P(w)\), and its minimum \(P(w^\star)\), i.e. \(G(w, v) \geq P(w) - P(w^\star)\). It is given by \(G(w, v) = P(w) - D(v)\) with dual objective function

subject to \(v \in ||X^Tv||_{\infty} \leq n_{\text{samples}}\alpha\). At optimum, the duality gap is zero, \(G(w^\star, v^\star) = 0\) (a property called strong duality). With (scaled) dual variable \(v = c r\), current residual \(r = y - Xw\) and dual scaling

the stopping criterion is

A clever method to speedup the coordinate descent algorithm is to screen features such that at optimum \(w_j = 0\). Gap safe screening rules are such a tool. Anywhere during the optimization algorithm, they can tell which feature we can safely exclude, i.e., set to zero with certainty.

References#

The first reference explains the coordinate descent solver used in scikit-learn, the others treat gap safe screening rules.

1.1.3.2. Setting regularization parameter#

The alpha parameter controls the degree of sparsity of the estimated

coefficients.

1.1.3.2.1. Using cross-validation#

scikit-learn exposes objects that set the Lasso alpha parameter by

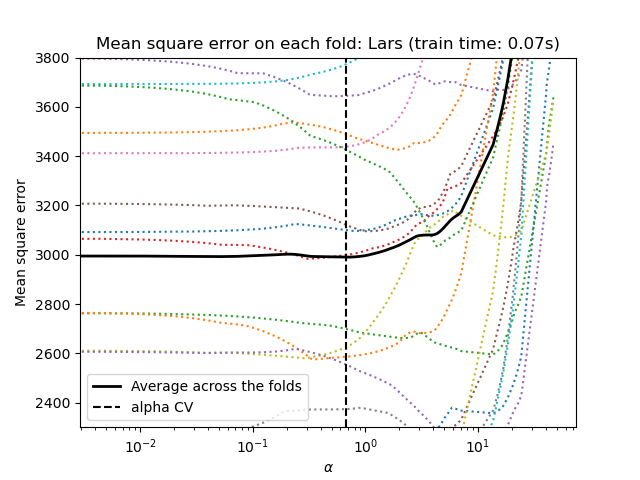

cross-validation: LassoCV and LassoLarsCV.

LassoLarsCV is based on the Least Angle Regression algorithm

explained below.

For high-dimensional datasets with many collinear features,

LassoCV is most often preferable. However, LassoLarsCV has

the advantage of exploring more relevant values of alpha parameter, and

if the number of samples is very small compared to the number of

features, it is often faster than LassoCV.

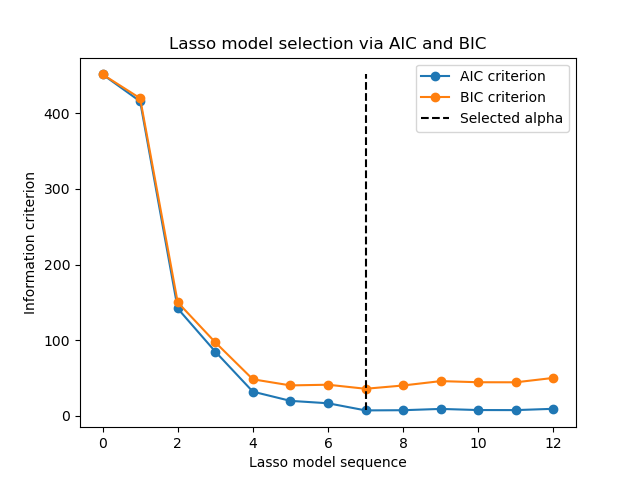

1.1.3.2.2. Information-criteria based model selection#

Alternatively, the estimator LassoLarsIC proposes to use the

Akaike information criterion (AIC) and the Bayes Information criterion (BIC).

It is a computationally cheaper alternative to find the optimal value of alpha

as the regularization path is computed only once instead of k+1 times

when using k-fold cross-validation.

Indeed, these criteria are computed on the in-sample training set. In short, they penalize the over-optimistic scores of the different Lasso models by their flexibility (cf. to “Mathematical details” section below).

However, such criteria need a proper estimation of the degrees of freedom of the solution, are derived for large samples (asymptotic results) and assume the correct model is candidates under investigation. They also tend to break when the problem is badly conditioned (e.g. more features than samples).

Examples

1.1.3.2.3. AIC and BIC criteria#

The definition of AIC (and thus BIC) might differ in the literature. In this section, we give more information regarding the criterion computed in scikit-learn.

Mathematical details#

The AIC criterion is defined as:

where \(\hat{L}\) is the maximum likelihood of the model and \(d\) is the number of parameters (as well referred to as degrees of freedom in the previous section).

The definition of BIC replaces the constant \(2\) by \(\log(N)\):

where \(N\) is the number of samples.

For a linear Gaussian model, the maximum log-likelihood is defined as:

where \(\sigma^2\) is an estimate of the noise variance, \(y_i\) and \(\hat{y}_i\) are respectively the true and predicted targets, and \(n\) is the number of samples.

Plugging the maximum log-likelihood in the AIC formula yields:

The first term of the above expression is sometimes discarded since it is a constant when \(\sigma^2\) is provided. In addition, it is sometimes stated that the AIC is equivalent to the \(C_p\) statistic [12]. In a strict sense, however, it is equivalent only up to some constant and a multiplicative factor.

At last, we mentioned above that \(\sigma^2\) is an estimate of the

noise variance. In LassoLarsIC when the parameter noise_variance is

not provided (default), the noise variance is estimated via the unbiased

estimator [13] defined as:

where \(p\) is the number of features and \(\hat{y}_i\) is the

predicted target using an ordinary least squares regression. Note, that this

formula is valid only when n_samples > n_features.

References

1.1.3.2.4. Comparison with the regularization parameter of SVM#

The equivalence between alpha and the regularization parameter of SVM,

C is given by alpha = 1 / C or alpha = 1 / (n_samples * C),

depending on the estimator and the exact objective function optimized by the

model.

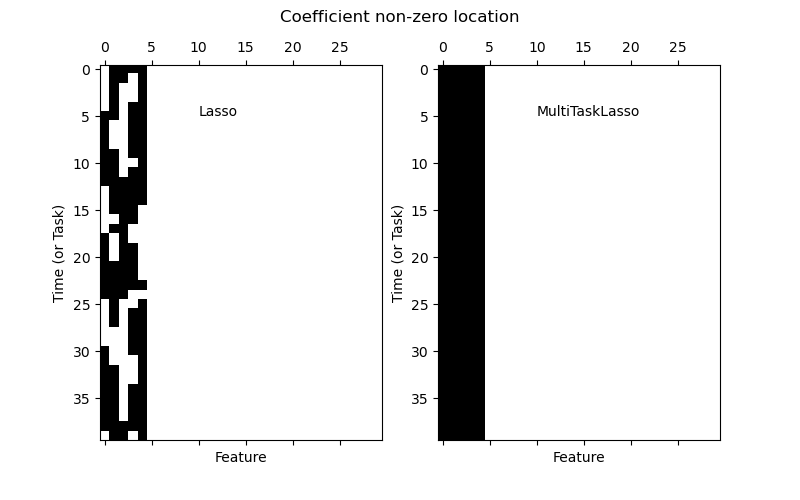

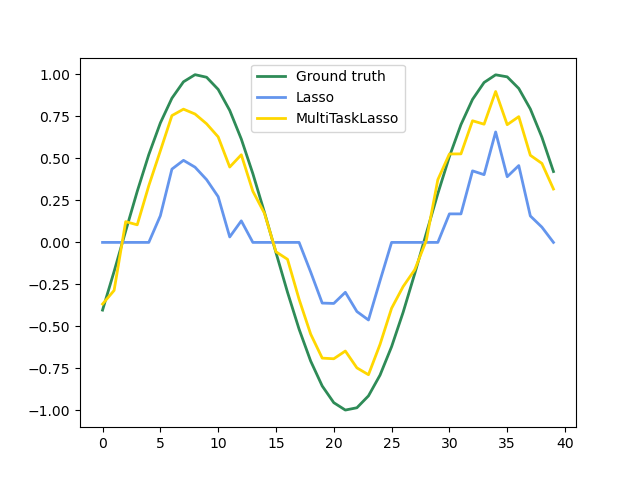

1.1.4. Multi-task Lasso#

The MultiTaskLasso is a linear model that estimates sparse

coefficients for multiple regression problems jointly: y is a 2D array,

of shape (n_samples, n_tasks). The constraint is that the selected

features are the same for all the regression problems, also called tasks.

The following figure compares the location of the non-zero entries in the coefficient matrix W obtained with a simple Lasso or a MultiTaskLasso. The Lasso estimates yield scattered non-zeros while the non-zeros of the MultiTaskLasso are full columns.

Fitting a time-series model, imposing that any active feature be active at all times.

Examples

Mathematical details#

Mathematically, it consists of a linear model trained with a mixed \(\ell_1\) \(\ell_2\)-norm for regularization. The objective function to minimize is:

where \(\text{Fro}\) indicates the Frobenius norm

and \(\ell_1\) \(\ell_2\) reads

The implementation in the class MultiTaskLasso uses

coordinate descent as the algorithm to fit the coefficients.

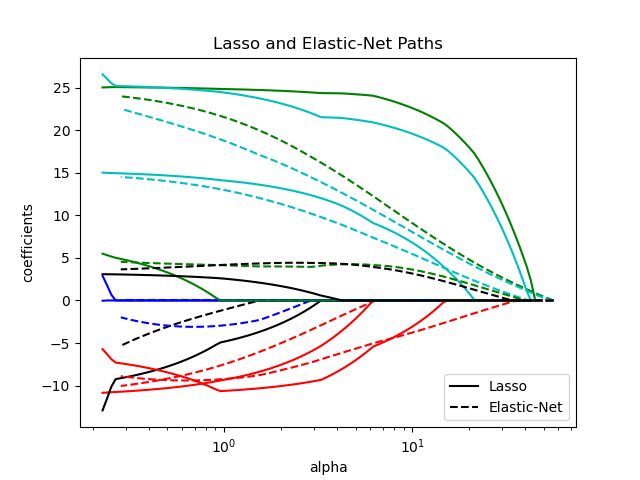

1.1.5. Elastic-Net#

ElasticNet is a linear regression model trained with both

\(\ell_1\) and \(\ell_2\)-norm regularization of the coefficients.

This combination allows for learning a sparse model where few of

the weights are non-zero like Lasso, while still maintaining

the regularization properties of Ridge. We control the convex

combination of \(\ell_1\) and \(\ell_2\) using the l1_ratio

parameter.

Elastic-net is useful when there are multiple features that are correlated with one another. Lasso is likely to pick one of these at random, while elastic-net is likely to pick both.

A practical advantage of trading-off between Lasso and Ridge is that it allows Elastic-Net to inherit some of Ridge’s stability under rotation.

The objective function to minimize is in this case

The class ElasticNetCV can be used to set the parameters

alpha (\(\alpha\)) and l1_ratio (\(\rho\)) by cross-validation.

Examples

References#

The following two references explain the iterations used in the coordinate descent solver of scikit-learn, as well as the duality gap computation used for convergence control.

“Regularization Path For Generalized linear Models by Coordinate Descent”, Friedman, Hastie & Tibshirani, J Stat Softw, 2010 (Paper).

“An Interior-Point Method for Large-Scale L1-Regularized Least Squares,” S. J. Kim, K. Koh, M. Lustig, S. Boyd and D. Gorinevsky, in IEEE Journal of Selected Topics in Signal Processing, 2007 (Paper)

1.1.6. Multi-task Elastic-Net#

The MultiTaskElasticNet is an elastic-net model that estimates sparse

coefficients for multiple regression problems jointly: Y is a 2D array

of shape (n_samples, n_tasks). The constraint is that the selected

features are the same for all the regression problems, also called tasks.

Mathematically, it consists of a linear model trained with a mixed \(\ell_1\) \(\ell_2\)-norm and \(\ell_2\)-norm for regularization. The objective function to minimize is:

The implementation in the class MultiTaskElasticNet uses coordinate descent as

the algorithm to fit the coefficients.

The class MultiTaskElasticNetCV can be used to set the parameters

alpha (\(\alpha\)) and l1_ratio (\(\rho\)) by cross-validation.

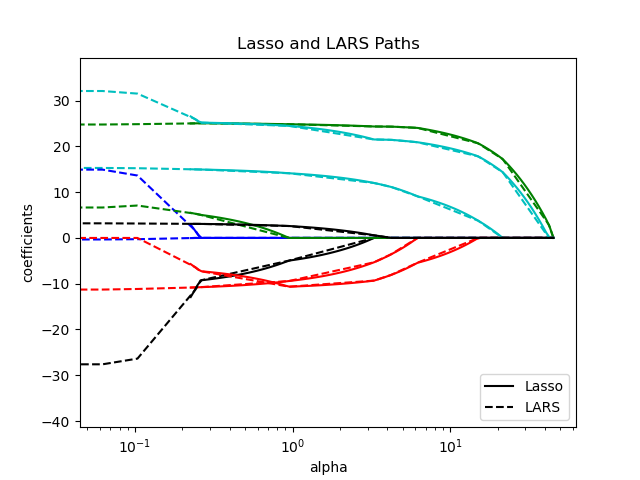

1.1.7. Least Angle Regression#

Least-angle regression (LARS) is a regression algorithm for high-dimensional data, developed by Bradley Efron, Trevor Hastie, Iain Johnstone and Robert Tibshirani. LARS is similar to forward stepwise regression. At each step, it finds the feature most correlated with the target. When there are multiple features having equal correlation, instead of continuing along the same feature, it proceeds in a direction equiangular between the features.

The advantages of LARS are:

It is numerically efficient in contexts where the number of features is significantly greater than the number of samples.

It is computationally just as fast as forward selection and has the same order of complexity as ordinary least squares.

It produces a full piecewise linear solution path, which is useful in cross-validation or similar attempts to tune the model.

If two features are almost equally correlated with the target, then their coefficients should increase at approximately the same rate. The algorithm thus behaves as intuition would expect, and also is more stable.

It is easily modified to produce solutions for other estimators, like the Lasso.

The disadvantages of the LARS method include:

Because LARS is based upon an iterative refitting of the residuals, it would appear to be especially sensitive to the effects of noise. This problem is discussed in detail by Weisberg in the discussion section of the Efron et al. (2004) Annals of Statistics article.

The LARS model can be used via the estimator Lars, or its

low-level implementation lars_path or lars_path_gram.

1.1.8. LARS Lasso#

LassoLars is a lasso model implemented using the LARS

algorithm, and unlike the implementation based on coordinate descent,

this yields the exact solution, which is piecewise linear as a

function of the norm of its coefficients.

>>> from sklearn import linear_model

>>> reg = linear_model.LassoLars(alpha=.1)

>>> reg.fit([[0, 0], [1, 1]], [0, 1])

LassoLars(alpha=0.1)

>>> reg.coef_

array([0.6, 0. ])

Examples

The LARS algorithm provides the full path of the coefficients along

the regularization parameter almost for free, thus a common operation

is to retrieve the path with one of the functions lars_path

or lars_path_gram.

Mathematical formulation#

The algorithm is similar to forward stepwise regression, but instead of including features at each step, the estimated coefficients are increased in a direction equiangular to each one’s correlations with the residual.

Instead of giving a vector result, the LARS solution consists of a

curve denoting the solution for each value of the \(\ell_1\) norm of the

parameter vector. The full coefficients path is stored in the array

coef_path_ of shape (n_features, max_features + 1). The first

column is always zero.

References

Original Algorithm is detailed in the paper Least Angle Regression by Hastie et al.

1.1.9. Orthogonal Matching Pursuit (OMP)#

OrthogonalMatchingPursuit and orthogonal_mp implement the OMP

algorithm for approximating the fit of a linear model with constraints imposed

on the number of non-zero coefficients (i.e. the \(\ell_0\) pseudo-norm).

Being a forward feature selection method like Least Angle Regression, orthogonal matching pursuit can approximate the optimum solution vector with a fixed number of non-zero elements:

Alternatively, orthogonal matching pursuit can target a specific error instead of a specific number of non-zero coefficients. This can be expressed as:

OMP is based on a greedy algorithm that includes at each step the atom most highly correlated with the current residual. It is similar to the simpler matching pursuit (MP) method, but better in that at each iteration, the residual is recomputed using an orthogonal projection on the space of the previously chosen dictionary elements.

Examples

References#

https://www.cs.technion.ac.il/~ronrubin/Publications/KSVD-OMP-v2.pdf

Matching pursuits with time-frequency dictionaries, S. G. Mallat, Z. Zhang, 1993.

1.1.10. Bayesian Regression#

Bayesian regression techniques can be used to include regularization parameters in the estimation procedure: the regularization parameter is not set in a hard sense but tuned to the data at hand.

This can be done by introducing uninformative priors

over the hyper parameters of the model.

The \(\ell_{2}\) regularization used in Ridge regression and classification is

equivalent to finding a maximum a posteriori estimation under a Gaussian prior

over the coefficients \(w\) with precision \(\lambda^{-1}\).

Instead of setting lambda manually, it is possible to treat it as a random

variable to be estimated from the data.

To obtain a fully probabilistic model, the output \(y\) is assumed to be Gaussian distributed around \(X w\):

where \(\alpha\) is again treated as a random variable that is to be estimated from the data.

The advantages of Bayesian Regression are:

It adapts to the data at hand.

It can be used to include regularization parameters in the estimation procedure.

The disadvantages of Bayesian regression include:

Inference of the model can be time consuming.

References#

A good introduction to Bayesian methods is given in C. Bishop: Pattern Recognition and Machine Learning.

Original Algorithm is detailed in the book Bayesian learning for neural networks by Radford M. Neal.

1.1.10.1. Bayesian Ridge Regression#

BayesianRidge estimates a probabilistic model of the

regression problem as described above.

The prior for the coefficient \(w\) is given by a spherical Gaussian:

The priors over \(\alpha\) and \(\lambda\) are chosen to be gamma

distributions, the

conjugate prior for the precision of the Gaussian. The resulting model is

called Bayesian Ridge Regression, and is similar to the classical

Ridge.

The parameters \(w\), \(\alpha\) and \(\lambda\) are estimated

jointly during the fit of the model, the regularization parameters

\(\alpha\) and \(\lambda\) being estimated by maximizing the

log marginal likelihood. The scikit-learn implementation

is based on the algorithm described in Appendix A of (Tipping, 2001)

where the update of the parameters \(\alpha\) and \(\lambda\) is done

as suggested in (MacKay, 1992). The initial value of the maximization procedure

can be set with the hyperparameters alpha_init and lambda_init.

There are four more hyperparameters, \(\alpha_1\), \(\alpha_2\), \(\lambda_1\) and \(\lambda_2\) of the gamma prior distributions over \(\alpha\) and \(\lambda\). These are usually chosen to be non-informative. By default \(\alpha_1 = \alpha_2 = \lambda_1 = \lambda_2 = 10^{-6}\).

Bayesian Ridge Regression is used for regression:

>>> from sklearn import linear_model

>>> X = [[0., 0.], [1., 1.], [2., 2.], [3., 3.]]

>>> Y = [0., 1., 2., 3.]

>>> reg = linear_model.BayesianRidge()

>>> reg.fit(X, Y)

BayesianRidge()

After being fitted, the model can then be used to predict new values:

>>> reg.predict([[1, 0.]])

array([0.50000013])

The coefficients \(w\) of the model can be accessed:

>>> reg.coef_

array([0.49999993, 0.49999993])

Due to the Bayesian framework, the weights found are slightly different from the ones found by Ordinary Least Squares. However, Bayesian Ridge Regression is more robust to ill-posed problems.

Examples

References#

Section 3.3 in Christopher M. Bishop: Pattern Recognition and Machine Learning, 2006

David J. C. MacKay, Bayesian Interpolation, 1992.

Michael E. Tipping, Sparse Bayesian Learning and the Relevance Vector Machine, 2001.

1.1.10.2. Automatic Relevance Determination - ARD#

The Automatic Relevance Determination (as being implemented in

ARDRegression) is a kind of linear model which is very similar to the

Bayesian Ridge Regression, but that leads to sparser coefficients \(w\)

[1] [2].

ARDRegression poses a different prior over \(w\): it drops

the spherical Gaussian distribution for a centered elliptic Gaussian

distribution. This means each coefficient \(w_{i}\) can itself be drawn from

a Gaussian distribution, centered on zero and with a precision

\(\lambda_{i}\):

with \(A\) being a positive definite diagonal matrix and \(\text{diag}(A) = \lambda = \{\lambda_{1},...,\lambda_{p}\}\).

In contrast to the Bayesian Ridge Regression, each coordinate of \(w_{i}\) has its own standard deviation \(\frac{1}{\lambda_i}\). The prior over all \(\lambda_i\) is chosen to be the same gamma distribution given by the hyperparameters \(\lambda_1\) and \(\lambda_2\).

ARD is also known in the literature as Sparse Bayesian Learning and Relevance Vector Machine [3] [4].

See Comparing Linear Bayesian Regressors for a worked-out comparison between ARD and Bayesian Ridge Regression.

See L1-based models for Sparse Signals for a comparison between various methods - Lasso, ARD and ElasticNet - on correlated data.

References

1.1.11. Logistic regression#

The logistic regression is implemented in LogisticRegression. Despite

its name, it is implemented as a linear model for classification rather than

regression in terms of the scikit-learn/ML nomenclature. The logistic

regression is also known in the literature as logit regression,

maximum-entropy classification (MaxEnt) or the log-linear classifier. In this

model, the probabilities describing the possible outcomes of a single trial

are modeled using a logistic function.

This implementation can fit binary, One-vs-Rest, or multinomial logistic regression with optional \(\ell_1\), \(\ell_2\) or Elastic-Net regularization.

Note

Regularization

Regularization is applied by default, which is common in machine learning but not in statistics. Another advantage of regularization is that it improves numerical stability. No regularization amounts to setting C to a very high value.

Note

Logistic Regression as a special case of the Generalized Linear Models (GLM)

Logistic regression is a special case of Generalized Linear Models with a Binomial / Bernoulli conditional distribution and a Logit link. The numerical output of the logistic regression, which is the predicted probability, can be used as a classifier by applying a threshold (by default 0.5) to it. This is how it is implemented in scikit-learn, so it expects a categorical target, making the Logistic Regression a classifier.

Examples

1.1.11.1. Binary Case#

For notational ease, we assume that the target \(y_i\) takes values in the

set \(\{0, 1\}\) for data point \(i\).

Once fitted, the predict_proba

method of LogisticRegression predicts

the probability of the positive class \(P(y_i=1|X_i)\) as

As an optimization problem, binary class logistic regression with regularization term \(r(w)\) minimizes the following cost function:

where \({s_i}\) corresponds to the weights assigned by the user to a specific training sample (the vector \(s\) is formed by element-wise multiplication of the class weights and sample weights), and the sum \(S = \sum_{i=1}^n s_i\).

We currently provide four choices for the regularization or penalty term \(r(w)\)

via the arguments C and l1_ratio:

penalty |

\(r(w)\) |

|---|---|

none ( |

\(0\) |

\(\ell_1\) ( |

\(\|w\|_1\) |

\(\ell_2\) ( |

\(\frac{1}{2}\|w\|_2^2 = \frac{1}{2}w^T w\) |

ElasticNet ( |

\(\frac{1 - \rho}{2}w^T w + \rho \|w\|_1\) |

For ElasticNet, \(\rho\) (which corresponds to the l1_ratio parameter)

controls the strength of \(\ell_1\) regularization vs. \(\ell_2\)

regularization. Elastic-Net is equivalent to \(\ell_1\) when

\(\rho = 1\) and equivalent to \(\ell_2\) when \(\rho=0\).

Note that the scale of the class weights and the sample weights will influence

the optimization problem. For instance, multiplying the sample weights by a

constant \(b>0\) is equivalent to multiplying the (inverse) regularization

strength C by \(b\).

1.1.11.2. Multinomial Case#

The binary case can be extended to \(K\) classes leading to the multinomial logistic regression, see also log-linear model.

Note

It is possible to parameterize a \(K\)-class classification model using only \(K-1\) weight vectors, leaving one class probability fully determined by the other class probabilities by leveraging the fact that all class probabilities must sum to one. We deliberately choose to overparameterize the model using \(K\) weight vectors for ease of implementation and to preserve the symmetrical inductive bias regarding ordering of classes, see [16]. This effect becomes especially important when using regularization. The choice of overparameterization can be detrimental for unpenalized models since then the solution may not be unique, as shown in [16].

Mathematical details#

Let \(y_i \in \{1, \ldots, K\}\) be the label (ordinal) encoded target variable for observation \(i\).

Instead of a single coefficient vector, we now have

a matrix of coefficients \(W\) where each row vector \(W_k\) corresponds to class

\(k\). We aim at predicting the class probabilities \(P(y_i=k|X_i)\) via

predict_proba as:

The objective for the optimization becomes

where \([P]\) represents the Iverson bracket which evaluates to \(0\) if \(P\) is false, otherwise it evaluates to \(1\).

Again, \(s_{ik}\) are the weights assigned by the user (multiplication of sample weights and class weights) with their sum \(S = \sum_{i=1}^n \sum_{k=0}^{K-1} s_{ik}\).

We currently provide four choices for the regularization or penalty term \(r(W)\)

via the arguments C and l1_ratio, where \(m\) is the number of features:

penalty |

\(r(W)\) |

|---|---|

none ( |

\(0\) |

\(\ell_1\) ( |

\(\|W\|_{1,1} = \sum_{i=1}^m\sum_{j=1}^{K}|W_{i,j}|\) |

\(\ell_2\) ( |

\(\frac{1}{2}\|W\|_F^2 = \frac{1}{2}\sum_{i=1}^m\sum_{j=1}^{K} W_{i,j}^2\) |

ElasticNet ( |

\(\frac{1 - \rho}{2}\|W\|_F^2 + \rho \|W\|_{1,1}\) |

1.1.11.3. Solvers#

The solvers implemented in the class LogisticRegression

are “lbfgs”, “liblinear”, “newton-cg”, “newton-cholesky”, “sag” and “saga”:

The following table summarizes the penalties and multinomial multiclass supported by each solver:

Solvers |

|||||||

Penalties |

‘lbfgs’ |

‘liblinear’ |

‘newton-cg’ |

‘newton-cholesky’ |

‘sag’ |

‘saga’ |

|

L2 penalty |

yes |

yes |

yes |

yes |

yes |

yes |

|

L1 penalty |

no |

yes |

no |

no |

no |

yes |

|

Elastic-Net (L1 + L2) |

no |

no |

no |

no |

no |

yes |

|

No penalty |

yes |

no |

yes |

yes |

yes |

yes |

|

Multiclass support |

|||||||

multinomial multiclass |

yes |

no |

yes |

yes |

yes |

yes |

|

Behaviors |

|||||||

Penalize the intercept (bad) |

no |

yes |

no |

no |

no |

no |

|

Faster for large datasets |

no |

no |

no |

no |

yes |

yes |

|

Robust to unscaled datasets |

yes |

yes |

yes |

yes |

no |

no |

|

The “lbfgs” solver is used by default for its robustness. For

n_samples >> n_features, “newton-cholesky” is a good choice and can reach high

precision (tiny tol values). For large datasets

the “saga” solver is usually faster (than “lbfgs”), in particular for low precision

(high tol).

For large dataset, you may also consider using SGDClassifier

with loss="log_loss", which might be even faster but requires more tuning.

1.1.11.3.1. Differences between solvers#

There might be a difference in the scores obtained between

LogisticRegression with solver=liblinear or

LinearSVC and the external liblinear library directly,

when fit_intercept=False and the fit coef_ (or) the data to be predicted

are zeroes. This is because for the sample(s) with decision_function zero,

LogisticRegression and LinearSVC predict the

negative class, while liblinear predicts the positive class. Note that a model

with fit_intercept=False and having many samples with decision_function

zero, is likely to be an underfit, bad model and you are advised to set

fit_intercept=True and increase the intercept_scaling.

Solvers’ details#

The solver “liblinear” uses a coordinate descent (CD) algorithm, and relies on the excellent C++ LIBLINEAR library, which is shipped with scikit-learn. However, the CD algorithm implemented in liblinear cannot learn a true multinomial (multiclass) model. If you still want to use “liblinear” on multiclass problems, you can use a “one-vs-rest” scheme

OneVsRestClassifier(LogisticRegression(solver="liblinear")), see:class:`~sklearn.multiclass.OneVsRestClassifier. Note that minimizing the multinomial loss is expected to give better calibrated results as compared to a “one-vs-rest” scheme. For \(\ell_1\) regularizationsklearn.svm.l1_min_callows to calculate the lower bound for C in order to get a non “null” (all feature weights to zero) model.The “lbfgs”, “newton-cg”, “newton-cholesky” and “sag” solvers only support \(\ell_2\) regularization or no regularization, and are found to converge faster for some high-dimensional data. These solvers (and “saga”) learn a true multinomial logistic regression model [5].

The “sag” solver uses Stochastic Average Gradient descent [6]. It is faster than other solvers for large datasets, when both the number of samples and the number of features are large.

The “saga” solver [7] is a variant of “sag” that also supports the non-smooth \(\ell_1\) penalty (

l1_ratio=1). This is therefore the solver of choice for sparse multinomial logistic regression. It is also the only solver that supports Elastic-Net (0 < l1_ratio < 1).The “lbfgs” is an optimization algorithm that approximates the Broyden–Fletcher–Goldfarb–Shanno algorithm [8], which belongs to quasi-Newton methods. As such, it can deal with a wide range of different training data and is therefore the default solver. Its performance, however, suffers on poorly scaled datasets and on datasets with one-hot encoded categorical features with rare categories.

The “newton-cholesky” solver is an exact Newton solver that calculates the Hessian matrix and solves the resulting linear system. It is a very good choice for

n_samples>>n_featuresand can reach high precision (tiny values oftol), but has a few shortcomings: Only \(\ell_2\) regularization is supported. Furthermore, because the Hessian matrix is explicitly computed, the memory usage has a quadratic dependency onn_featuresas well as onn_classes.

For a comparison of some of these solvers, see [9].

References

Note

Feature selection with sparse logistic regression

A logistic regression with \(\ell_1\) penalty yields sparse models, and can thus be used to perform feature selection, as detailed in L1-based feature selection.

Note

P-value estimation

It is possible to obtain the p-values and confidence intervals for coefficients in cases of regression without penalization. The statsmodels package natively supports this. Within sklearn, one could use bootstrapping instead as well.

LogisticRegressionCV implements Logistic Regression with built-in

cross-validation support, to find the optimal C and l1_ratio parameters

according to the scoring attribute. The “newton-cg”, “sag”, “saga” and

“lbfgs” solvers are found to be faster for high-dimensional dense data, due

to warm-starting (see Glossary).

1.1.12. Generalized Linear Models#

Generalized Linear Models (GLM) extend linear models in two ways [10]. First, the predicted values \(\hat{y}\) are linked to a linear combination of the input variables \(X\) via an inverse link function \(h\) as

Secondly, the squared loss function is replaced by the unit deviance \(d\) of a distribution in the exponential family (or more precisely, a reproductive exponential dispersion model (EDM) [11]).

The minimization problem becomes:

where \(\alpha\) is the L2 regularization penalty. When sample weights are provided, the average becomes a weighted average.

The following table lists some specific EDMs and their unit deviance :

Distribution |

Target Domain |

Unit Deviance \(d(y, \hat{y})\) |

|---|---|---|

Normal |

\(y \in (-\infty, \infty)\) |

\((y-\hat{y})^2\) |

Bernoulli |

\(y \in \{0, 1\}\) |

\(2({y}\log\frac{y}{\hat{y}}+({1}-{y})\log\frac{{1}-{y}}{{1}-\hat{y}})\) |

Categorical |

\(y \in \{0, 1, ..., k\}\) |

\(2\sum_{i \in \{0, 1, ..., k\}} I(y = i) y_\text{i}\log\frac{I(y = i)}{\hat{I(y = i)}}\) |

Poisson |

\(y \in [0, \infty)\) |

\(2(y\log\frac{y}{\hat{y}}-y+\hat{y})\) |

Gamma |

\(y \in (0, \infty)\) |

\(2(\log\frac{\hat{y}}{y}+\frac{y}{\hat{y}}-1)\) |

Inverse Gaussian |

\(y \in (0, \infty)\) |

\(\frac{(y-\hat{y})^2}{y\hat{y}^2}\) |

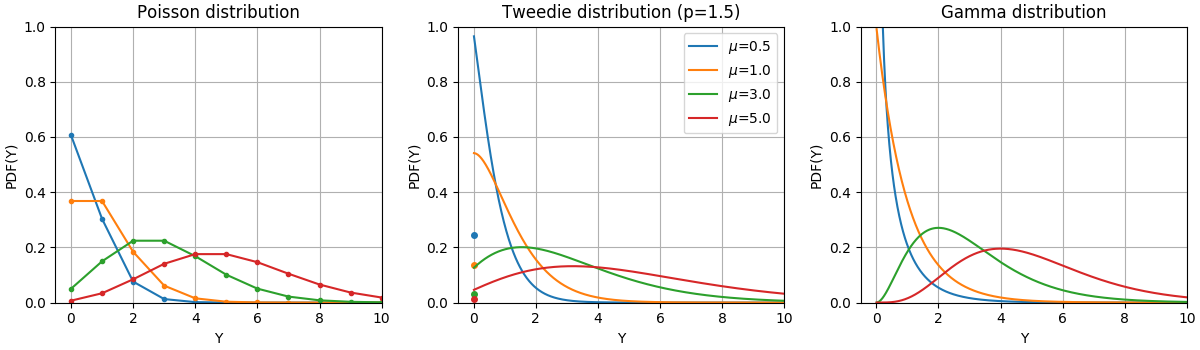

The Probability Density Functions (PDF) of these distributions are illustrated in the following figure,

PDF of a random variable Y following Poisson, Tweedie (power=1.5) and Gamma distributions with different mean values (\(\mu\)). Observe the point mass at \(Y=0\) for the Poisson distribution and the Tweedie (power=1.5) distribution, but not for the Gamma distribution which has a strictly positive target domain.#

The Bernoulli distribution is a discrete probability distribution modelling a Bernoulli trial - an event that has only two mutually exclusive outcomes. The Categorical distribution is a generalization of the Bernoulli distribution for a categorical random variable. While a random variable in a Bernoulli distribution has two possible outcomes, a Categorical random variable can take on one of K possible categories, with the probability of each category specified separately.

The choice of the distribution depends on the problem at hand:

If the target values \(y\) are counts (non-negative integer valued) or relative frequencies (non-negative), you might use a Poisson distribution with a log-link.

If the target values are positive valued and skewed, you might try a Gamma distribution with a log-link.

If the target values seem to be heavier tailed than a Gamma distribution, you might try an Inverse Gaussian distribution (or even higher variance powers of the Tweedie family).

If the target values \(y\) are probabilities, you can use the Bernoulli distribution. The Bernoulli distribution with a logit link can be used for binary classification. The Categorical distribution with a softmax link can be used for multiclass classification.

Examples of use cases#

Agriculture / weather modeling: number of rain events per year (Poisson), amount of rainfall per event (Gamma), total rainfall per year (Tweedie / Compound Poisson Gamma).

Risk modeling / insurance policy pricing: number of claim events / policyholder per year (Poisson), cost per event (Gamma), total cost per policyholder per year (Tweedie / Compound Poisson Gamma).

Credit Default: probability that a loan can’t be paid back (Bernoulli).

Fraud Detection: probability that a financial transaction like a cash transfer is a fraudulent transaction (Bernoulli).

Predictive maintenance: number of production interruption events per year (Poisson), duration of interruption (Gamma), total interruption time per year (Tweedie / Compound Poisson Gamma).

Medical Drug Testing: probability of curing a patient in a set of trials or probability that a patient will experience side effects (Bernoulli).

News Classification: classification of news articles into three categories namely Business News, Politics and Entertainment news (Categorical).

References

1.1.12.1. Usage#

TweedieRegressor implements a generalized linear model for the

Tweedie distribution, that allows to model any of the above mentioned

distributions using the appropriate power parameter. In particular:

power = 0: Normal distribution. Specific estimators such asRidge,ElasticNetare generally more appropriate in this case.power = 1: Poisson distribution.PoissonRegressoris exposed for convenience. However, it is strictly equivalent toTweedieRegressor(power=1, link='log').power = 2: Gamma distribution.GammaRegressoris exposed for convenience. However, it is strictly equivalent toTweedieRegressor(power=2, link='log').power = 3: Inverse Gaussian distribution.

The link function is determined by the link parameter.

Usage example:

>>> from sklearn.linear_model import TweedieRegressor

>>> reg = TweedieRegressor(power=1, alpha=0.5, link='log')

>>> reg.fit([[0, 0], [0, 1], [2, 2]], [0, 1, 2])

TweedieRegressor(alpha=0.5, link='log', power=1)

>>> reg.coef_

array([0.2463, 0.4337])

>>> reg.intercept_

np.float64(-0.7638)

Examples

Practical considerations#

The feature matrix X should be standardized before fitting. This ensures

that the penalty treats features equally.

Since the linear predictor \(Xw\) can be negative and Poisson,

Gamma and Inverse Gaussian distributions don’t support negative values, it

is necessary to apply an inverse link function that guarantees the

non-negativeness. For example with link='log', the inverse link function

becomes \(h(Xw)=\exp(Xw)\).

If you want to model a relative frequency, i.e. counts per exposure (time, volume, …) you can do so by using a Poisson distribution and passing \(y=\frac{\mathrm{counts}}{\mathrm{exposure}}\) as target values together with \(\mathrm{exposure}\) as sample weights. For a concrete example see e.g. Tweedie regression on insurance claims.

When performing cross-validation for the power parameter of

TweedieRegressor, it is advisable to specify an explicit scoring function,

because the default scorer TweedieRegressor.score is a function of

power itself.

1.1.13. Stochastic Gradient Descent - SGD#

Stochastic gradient descent is a simple yet very efficient approach

to fit linear models. It is particularly useful when the number of samples

(and the number of features) is very large.

The partial_fit method allows online/out-of-core learning.

The classes SGDClassifier and SGDRegressor provide

functionality to fit linear models for classification and regression

using different (convex) loss functions and different penalties.

E.g., with loss="log", SGDClassifier

fits a logistic regression model,

while with loss="hinge" it fits a linear support vector machine (SVM).

You can refer to the dedicated Stochastic Gradient Descent documentation section for more details.

1.1.13.1. Perceptron#

The Perceptron is another simple classification algorithm suitable for

large scale learning and derives from SGD. By default:

It does not require a learning rate.

It is not regularized (penalized).

It updates its model only on mistakes.

The last characteristic implies that the Perceptron is slightly faster to train than SGD with the hinge loss and that the resulting models are sparser.

In fact, the Perceptron is a wrapper around the SGDClassifier

class using a perceptron loss and a constant learning rate. Refer to

mathematical section of the SGD procedure

for more details.

1.1.13.2. Passive Aggressive Algorithms#

The passive-aggressive (PA) algorithms are another family of 2 algorithms (PA-I and

PA-II) for large-scale online learning that derive from SGD. They are similar to the

Perceptron in that they do not require a learning rate. However, contrary to the

Perceptron, they include a regularization parameter eta0 (\(C\) in the

reference paper).

For classification,

SGDClassifier(loss="hinge", penalty=None, learning_rate="pa1", eta0=1.0) can

be used for PA-I or with learning_rate="pa2" for PA-II. For regression,

SGDRegressor(loss="epsilon_insensitive", penalty=None, learning_rate="pa1",

eta0=1.0) can be used for PA-I or with learning_rate="pa2" for PA-II.

References#

“Online Passive-Aggressive Algorithms” K. Crammer, O. Dekel, J. Keshat, S. Shalev-Shwartz, Y. Singer - JMLR 7 (2006)

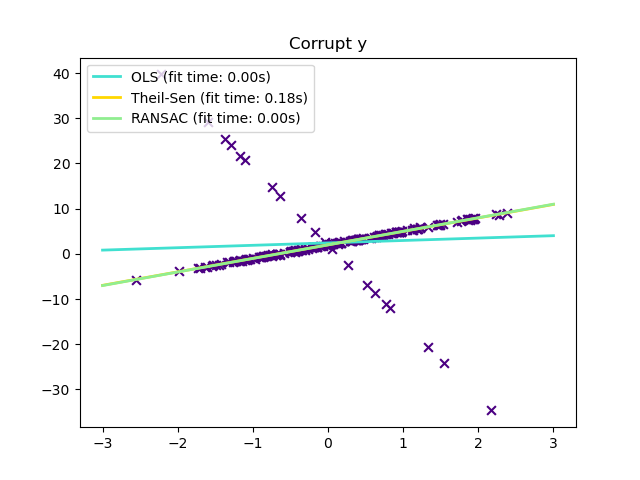

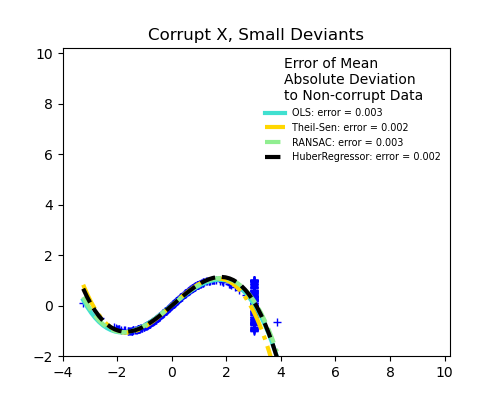

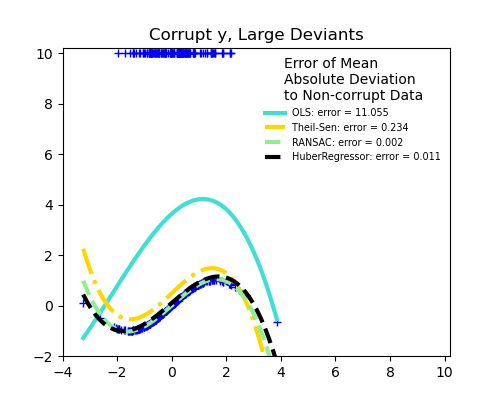

1.1.14. Robustness regression: outliers and modeling errors#

Robust regression aims to fit a regression model in the presence of corrupt data: either outliers, or error in the model.

1.1.14.1. Different scenario and useful concepts#

There are different things to keep in mind when dealing with data corrupted by outliers:

Outliers in X or in y?

Outliers in the y direction

Outliers in the X direction

Fraction of outliers versus amplitude of error

The number of outlying points matters, but also how much they are outliers.

Small outliers

Large outliers

An important notion of robust fitting is that of breakdown point: the fraction of data that can be outlying for the fit to start missing the inlying data.

Note that in general, robust fitting in high-dimensional setting (large

n_features) is very hard. The robust models here will probably not work

in these settings.

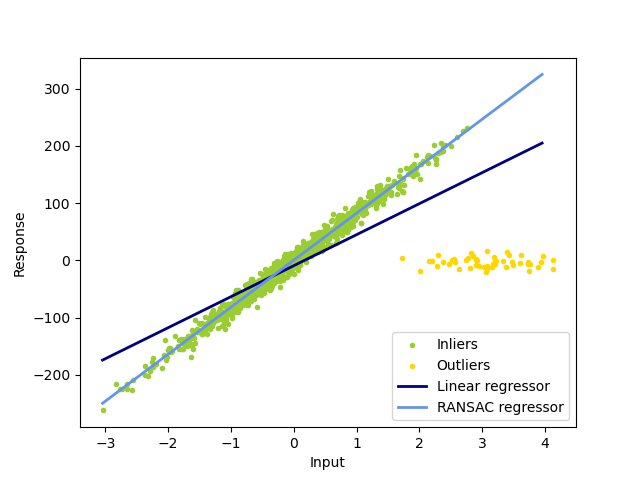

1.1.14.2. RANSAC: RANdom SAmple Consensus#

RANSAC (RANdom SAmple Consensus) fits a model from random subsets of inliers from the complete data set.

RANSAC is a non-deterministic algorithm producing only a reasonable result with

a certain probability, which is dependent on the number of iterations (see

max_trials parameter). It is typically used for linear and non-linear

regression problems and is especially popular in the field of photogrammetric

computer vision.

The algorithm splits the complete input sample data into a set of inliers, which may be subject to noise, and outliers, which are e.g. caused by erroneous measurements or invalid hypotheses about the data. The resulting model is then estimated only from the determined inliers.

Examples

Details of the algorithm#

Each iteration performs the following steps:

Select

min_samplesrandom samples from the original data and check whether the set of data is valid (seeis_data_valid).Fit a model to the random subset (

estimator.fit) and check whether the estimated model is valid (seeis_model_valid).Classify all data as inliers or outliers by calculating the residuals to the estimated model (

estimator.predict(X) - y) - all data samples with absolute residuals smaller than or equal to theresidual_thresholdare considered as inliers.Save fitted model as best model if number of inlier samples is maximal. In case the current estimated model has the same number of inliers, it is only considered as the best model if it has better score.

These steps are performed either a maximum number of times (max_trials) or

until one of the special stop criteria are met (see stop_n_inliers and

stop_score). The final model is estimated using all inlier samples (consensus

set) of the previously determined best model.

The is_data_valid and is_model_valid functions allow to identify and reject

degenerate combinations of random sub-samples. If the estimated model is not

needed for identifying degenerate cases, is_data_valid should be used as it

is called prior to fitting the model and thus leading to better computational

performance.

References#

“Random Sample Consensus: A Paradigm for Model Fitting with Applications to Image Analysis and Automated Cartography” Martin A. Fischler and Robert C. Bolles - SRI International (1981)

“Performance Evaluation of RANSAC Family” Sunglok Choi, Taemin Kim and Wonpil Yu - BMVC (2009)

1.1.14.3. Theil-Sen estimator: generalized-median-based estimator#

The TheilSenRegressor estimator uses a generalization of the median in

multiple dimensions. It is thus robust to multivariate outliers. Note however

that the robustness of the estimator decreases quickly with the dimensionality

of the problem. It loses its robustness properties and becomes no

better than an ordinary least squares in high dimension.

Examples

Theoretical considerations#

TheilSenRegressor is comparable to the Ordinary Least Squares

(OLS) in terms of asymptotic efficiency and as an

unbiased estimator. In contrast to OLS, Theil-Sen is a non-parametric

method which means it makes no assumption about the underlying

distribution of the data. Since Theil-Sen is a median-based estimator, it

is more robust against corrupted data aka outliers. In univariate

setting, Theil-Sen has a breakdown point of about 29.3% in case of a

simple linear regression which means that it can tolerate arbitrary

corrupted data of up to 29.3%.

The implementation of TheilSenRegressor in scikit-learn follows a

generalization to a multivariate linear regression model [14] using the

spatial median which is a generalization of the median to multiple

dimensions [15].

In terms of time and space complexity, Theil-Sen scales according to

which makes it infeasible to be applied exhaustively to problems with a large number of samples and features. Therefore, the magnitude of a subpopulation can be chosen to limit the time and space complexity by considering only a random subset of all possible combinations.

References

Also see the Wikipedia page

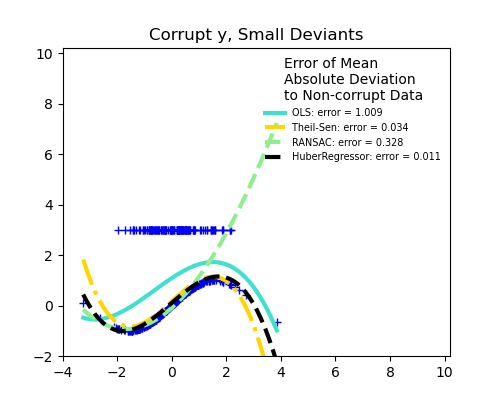

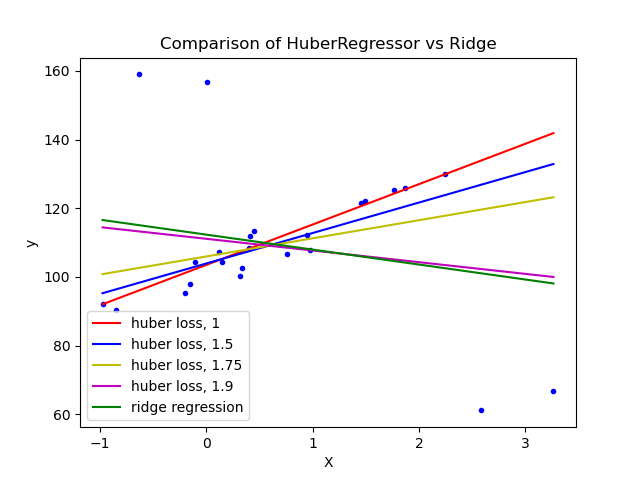

1.1.14.4. Huber Regression#

The HuberRegressor is different from Ridge because it applies a

linear loss to samples that are defined as outliers by the epsilon parameter.

A sample is classified as an inlier if the absolute error of that sample is

less than the threshold epsilon. It differs from TheilSenRegressor

and RANSACRegressor because it does not ignore the effect of the outliers

but gives a lesser weight to them.

Examples

Mathematical details#

HuberRegressor minimizes

where the loss function is given by

It is advised to set the parameter epsilon to 1.35 to achieve 95%

statistical efficiency.

References

Peter J. Huber, Elvezio M. Ronchetti: Robust Statistics, Concomitant scale estimates, p. 172.

The HuberRegressor differs from using SGDRegressor with loss set to huber

in the following ways.

HuberRegressoris scaling invariant. Onceepsilonis set, scalingXandydown or up by different values would produce the same robustness to outliers as before. as compared toSGDRegressorwhereepsilonhas to be set again whenXandyare scaled.HuberRegressorshould be more efficient to use on data with small number of samples whileSGDRegressorneeds a number of passes on the training data to produce the same robustness.

Note that this estimator is different from the R implementation of Robust Regression because the R implementation does a weighted least squares implementation with weights given to each sample on the basis of how much the residual is greater than a certain threshold.

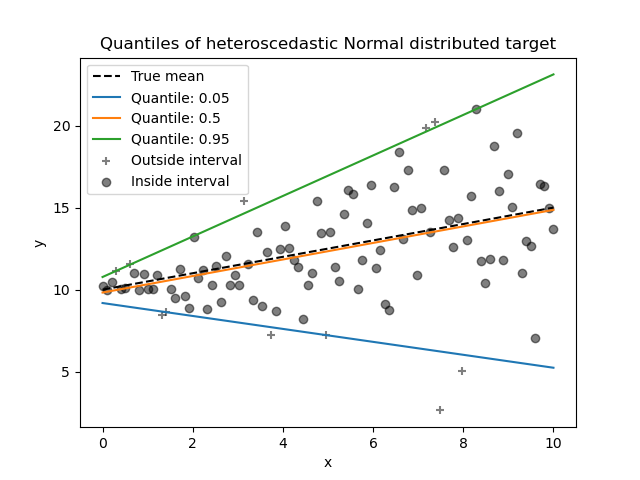

1.1.15. Quantile Regression#

Quantile regression estimates the median or other quantiles of \(y\) conditional on \(X\), while ordinary least squares (OLS) estimates the conditional mean.

Quantile regression may be useful if one is interested in predicting an interval instead of point prediction. Sometimes, prediction intervals are calculated based on the assumption that prediction error is distributed normally with zero mean and constant variance. Quantile regression provides sensible prediction intervals even for errors with non-constant (but predictable) variance or non-normal distribution.

Based on minimizing the pinball loss, conditional quantiles can also be

estimated by models other than linear models. For example,

GradientBoostingRegressor can predict conditional

quantiles if its parameter loss is set to "quantile" and parameter

alpha is set to the quantile that should be predicted. See the example in

Prediction Intervals for Gradient Boosting Regression.

Most implementations of quantile regression are based on linear programming

problem. The current implementation is based on

scipy.optimize.linprog.

Examples

Mathematical details#

As a linear model, the QuantileRegressor gives linear predictions

\(\hat{y}(w, X) = Xw\) for the \(q\)-th quantile, \(q \in (0, 1)\).

The weights or coefficients \(w\) are then found by the following

minimization problem:

This consists of the pinball loss (also known as linear loss),

see also mean_pinball_loss,

and the L1 penalty controlled by parameter alpha, similar to

Lasso.

As the pinball loss is only linear in the residuals, quantile regression is

much more robust to outliers than squared error based estimation of the mean.

Somewhat in between is the HuberRegressor.

References#

Koenker, R., & Bassett Jr, G. (1978). Regression quantiles. Econometrica: journal of the Econometric Society, 33-50.

Portnoy, S., & Koenker, R. (1997). The Gaussian hare and the Laplacian tortoise: computability of squared-error versus absolute-error estimators. Statistical Science, 12, 279-300.

Koenker, R. (2005). Quantile Regression. Cambridge University Press.

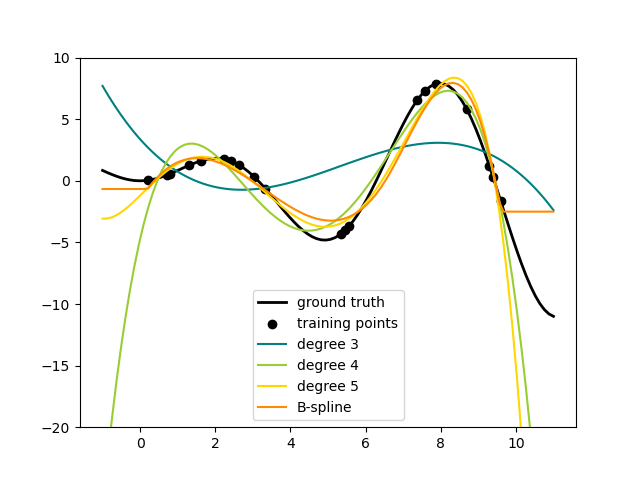

1.1.16. Polynomial regression: extending linear models with basis functions#

One common pattern within machine learning is to use linear models trained on nonlinear functions of the data. This approach maintains the generally fast performance of linear methods, while allowing them to fit a much wider range of data.

Mathematical details#

For example, a simple linear regression can be extended by constructing polynomial features from the coefficients. In the standard linear regression case, you might have a model that looks like this for two-dimensional data:

If we want to fit a paraboloid to the data instead of a plane, we can combine the features in second-order polynomials, so that the model looks like this:

The (sometimes surprising) observation is that this is still a linear model: to see this, imagine creating a new set of features

With this re-labeling of the data, our problem can be written

We see that the resulting polynomial regression is in the same class of linear models we considered above (i.e. the model is linear in \(w\)) and can be solved by the same techniques. By considering linear fits within a higher-dimensional space built with these basis functions, the model has the flexibility to fit a much broader range of data.

Here is an example of applying this idea to one-dimensional data, using polynomial features of varying degrees:

This figure is created using the PolynomialFeatures transformer, which

transforms an input data matrix into a new data matrix of a given degree.

It can be used as follows:

>>> from sklearn.preprocessing import PolynomialFeatures

>>> import numpy as np

>>> X = np.arange(6).reshape(3, 2)

>>> X

array([[0, 1],

[2, 3],

[4, 5]])

>>> poly = PolynomialFeatures(degree=2)

>>> poly.fit_transform(X)

array([[ 1., 0., 1., 0., 0., 1.],

[ 1., 2., 3., 4., 6., 9.],

[ 1., 4., 5., 16., 20., 25.]])

The features of X have been transformed from \([x_1, x_2]\) to

\([1, x_1, x_2, x_1^2, x_1 x_2, x_2^2]\), and can now be used within

any linear model.

This sort of preprocessing can be streamlined with the Pipeline tools. A single object representing a simple polynomial regression can be created and used as follows:

>>> from sklearn.preprocessing import PolynomialFeatures

>>> from sklearn.linear_model import LinearRegression

>>> from sklearn.pipeline import Pipeline

>>> import numpy as np

>>> model = Pipeline([('poly', PolynomialFeatures(degree=3)),

... ('linear', LinearRegression(fit_intercept=False))])

>>> # fit to an order-3 polynomial data

>>> x = np.arange(5)

>>> y = 3 - 2 * x + x ** 2 - x ** 3

>>> model = model.fit(x[:, np.newaxis], y)

>>> model.named_steps['linear'].coef_

array([ 3., -2., 1., -1.])

The linear model trained on polynomial features is able to exactly recover the input polynomial coefficients.

In some cases it’s not necessary to include higher powers of any single feature,

but only the so-called interaction features

that multiply together at most \(d\) distinct features.

These can be gotten from PolynomialFeatures with the setting

interaction_only=True.

For example, when dealing with boolean features, \(x_i^n = x_i\) for all \(n\) and is therefore useless; but \(x_i x_j\) represents the conjunction of two booleans. This way, we can solve the XOR problem with a linear classifier:

>>> from sklearn.linear_model import Perceptron

>>> from sklearn.preprocessing import PolynomialFeatures

>>> import numpy as np

>>> X = np.array([[0, 0], [0, 1], [1, 0], [1, 1]])

>>> y = X[:, 0] ^ X[:, 1]

>>> y

array([0, 1, 1, 0])

>>> X = PolynomialFeatures(interaction_only=True).fit_transform(X).astype(int)

>>> X

array([[1, 0, 0, 0],

[1, 0, 1, 0],

[1, 1, 0, 0],

[1, 1, 1, 1]])

>>> clf = Perceptron(fit_intercept=False, max_iter=10, tol=None,

... shuffle=False).fit(X, y)

And the classifier “predictions” are perfect:

>>> clf.predict(X)

array([0, 1, 1, 0])

>>> clf.score(X, y)

1.0