Note

Go to the end to download the full example code. or to run this example in your browser via JupyterLite or Binder

Combine predictors using stacking#

Stacking refers to a method to blend estimators. In this strategy, some estimators are individually fitted on some training data while a final estimator is trained using the stacked predictions of these base estimators.

In this example, we illustrate the use case in which different regressors are stacked together and a final linear penalized regressor is used to output the prediction. We compare the performance of each individual regressor with the stacking strategy. Stacking slightly improves the overall performance.

# Authors: The scikit-learn developers

# SPDX-License-Identifier: BSD-3-Clause

Download the dataset#

We will use the Ames Housing dataset which was first compiled by Dean De Cock and became better known after it was used in Kaggle challenge. It is a set of 1460 residential homes in Ames, Iowa, each described by 80 features. We will use it to predict the final logarithmic price of the houses. In this example we will use only 20 most interesting features chosen using GradientBoostingRegressor() and limit number of entries (here we won’t go into the details on how to select the most interesting features).

The Ames housing dataset is not shipped with scikit-learn and therefore we will fetch it from OpenML.

import numpy as np

from sklearn.datasets import fetch_openml

from sklearn.utils import shuffle

def load_ames_housing():

df = fetch_openml(name="house_prices", as_frame=True)

X = df.data

y = df.target

features = [

"YrSold",

"HeatingQC",

"Street",

"YearRemodAdd",

"Heating",

"MasVnrType",

"BsmtUnfSF",

"Foundation",

"MasVnrArea",

"MSSubClass",

"ExterQual",

"Condition2",

"GarageCars",

"GarageType",

"OverallQual",

"TotalBsmtSF",

"BsmtFinSF1",

"HouseStyle",

"MiscFeature",

"MoSold",

]

X = X.loc[:, features]

X, y = shuffle(X, y, random_state=0)

X = X.iloc[:600]

y = y.iloc[:600]

return X, np.log(y)

X, y = load_ames_housing()

Make pipeline to preprocess the data#

Before we can use Ames dataset we still need to do some preprocessing. First, we will select the categorical and numerical columns of the dataset to construct the first step of the pipeline.

from sklearn.compose import make_column_selector

cat_selector = make_column_selector(dtype_include=object)

num_selector = make_column_selector(dtype_include=np.number)

cat_selector(X)

['HeatingQC', 'Street', 'Heating', 'MasVnrType', 'Foundation', 'ExterQual', 'Condition2', 'GarageType', 'HouseStyle', 'MiscFeature']

num_selector(X)

['YrSold', 'YearRemodAdd', 'BsmtUnfSF', 'MasVnrArea', 'MSSubClass', 'GarageCars', 'OverallQual', 'TotalBsmtSF', 'BsmtFinSF1', 'MoSold']

Then, we will need to design preprocessing pipelines which depends on the ending regressor. If the ending regressor is a linear model, one needs to one-hot encode the categories. If the ending regressor is a tree-based model an ordinal encoder will be sufficient. Besides, numerical values need to be standardized for a linear model while the raw numerical data can be treated as is by a tree-based model. However, both models need an imputer to handle missing values.

We will first design the pipeline required for the tree-based models.

from sklearn.compose import make_column_transformer

from sklearn.impute import SimpleImputer

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import OrdinalEncoder

cat_tree_processor = OrdinalEncoder(

handle_unknown="use_encoded_value",

unknown_value=-1,

encoded_missing_value=-2,

)

num_tree_processor = SimpleImputer(strategy="mean", add_indicator=True)

tree_preprocessor = make_column_transformer(

(num_tree_processor, num_selector), (cat_tree_processor, cat_selector)

)

tree_preprocessor

Then, we will now define the preprocessor used when the ending regressor is a linear model.

from sklearn.preprocessing import OneHotEncoder, StandardScaler

cat_linear_processor = OneHotEncoder(handle_unknown="ignore")

num_linear_processor = make_pipeline(

StandardScaler(), SimpleImputer(strategy="mean", add_indicator=True)

)

linear_preprocessor = make_column_transformer(

(num_linear_processor, num_selector), (cat_linear_processor, cat_selector)

)

linear_preprocessor

Stack of predictors on a single data set#

It is sometimes tedious to find the model which will best perform on a given dataset. Stacking provide an alternative by combining the outputs of several learners, without the need to choose a model specifically. The performance of stacking is usually close to the best model and sometimes it can outperform the prediction performance of each individual model.

Here, we combine 3 learners (linear and non-linear) and use a ridge regressor to combine their outputs together.

Note

Although we will make new pipelines with the processors which we wrote in

the previous section for the 3 learners, the final estimator

RidgeCV() does not need preprocessing of

the data as it will be fed with the already preprocessed output from the 3

learners.

from sklearn.linear_model import LassoCV

lasso_pipeline = make_pipeline(linear_preprocessor, LassoCV())

lasso_pipeline

from sklearn.ensemble import RandomForestRegressor

rf_pipeline = make_pipeline(tree_preprocessor, RandomForestRegressor(random_state=42))

rf_pipeline

from sklearn.ensemble import HistGradientBoostingRegressor

gbdt_pipeline = make_pipeline(

tree_preprocessor, HistGradientBoostingRegressor(random_state=0)

)

gbdt_pipeline

from sklearn.ensemble import StackingRegressor

from sklearn.linear_model import RidgeCV

estimators = [

("Random Forest", rf_pipeline),

("Lasso", lasso_pipeline),

("Gradient Boosting", gbdt_pipeline),

]

stacking_regressor = StackingRegressor(estimators=estimators, final_estimator=RidgeCV())

stacking_regressor

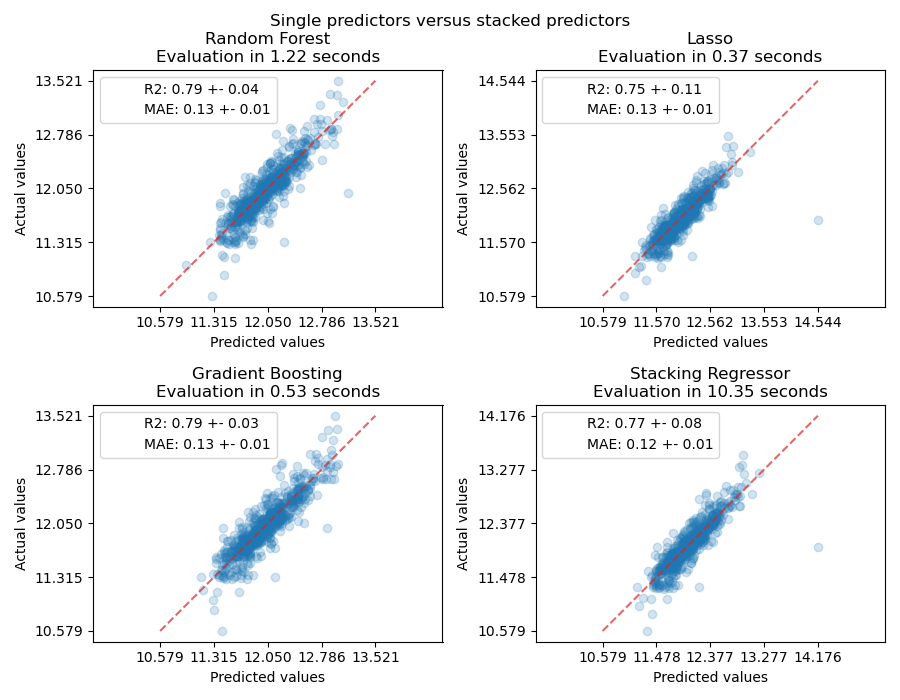

Measure and plot the results#

Now we can use Ames Housing dataset to make the predictions. We check the performance of each individual predictor as well as of the stack of the regressors.

import time

import matplotlib.pyplot as plt

from sklearn.metrics import PredictionErrorDisplay

from sklearn.model_selection import cross_val_predict, cross_validate

fig, axs = plt.subplots(2, 2, figsize=(9, 7))

axs = np.ravel(axs)

for ax, (name, est) in zip(

axs, estimators + [("Stacking Regressor", stacking_regressor)]

):

scorers = {"R2": "r2", "MAE": "neg_mean_absolute_error"}

start_time = time.time()

scores = cross_validate(

est, X, y, scoring=list(scorers.values()), n_jobs=-1, verbose=0

)

elapsed_time = time.time() - start_time

y_pred = cross_val_predict(est, X, y, n_jobs=-1, verbose=0)

scores = {

key: (

f"{np.abs(np.mean(scores[f'test_{value}'])):.2f} +- "

f"{np.std(scores[f'test_{value}']):.2f}"

)

for key, value in scorers.items()

}

display = PredictionErrorDisplay.from_predictions(

y_true=y,

y_pred=y_pred,

kind="actual_vs_predicted",

ax=ax,

scatter_kwargs={"alpha": 0.2, "color": "tab:blue"},

line_kwargs={"color": "tab:red"},

)

ax.set_title(f"{name}\nEvaluation in {elapsed_time:.2f} seconds")

for name, score in scores.items():

ax.plot([], [], " ", label=f"{name}: {score}")

ax.legend(loc="upper left")

plt.suptitle("Single predictors versus stacked predictors")

plt.tight_layout()

plt.subplots_adjust(top=0.9)

plt.show()

The stacked regressor will combine the strengths of the different regressors. However, we also see that training the stacked regressor is much more computationally expensive.

Total running time of the script: (0 minutes 25.547 seconds)

Related examples