Note

Go to the end to download the full example code or to run this example in your browser via JupyterLite or Binder

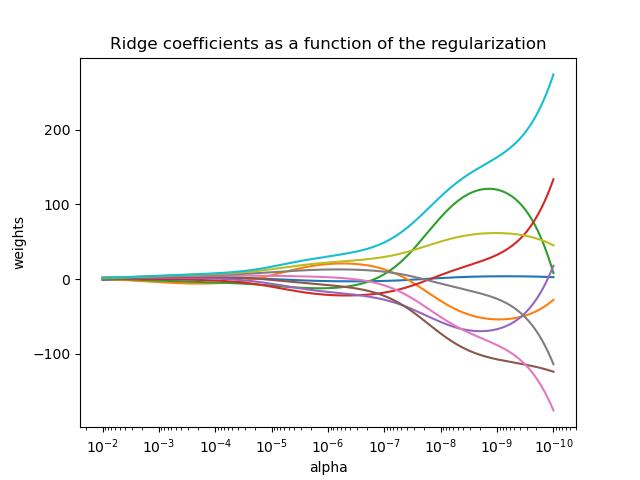

Plot Ridge coefficients as a function of the regularization¶

Shows the effect of collinearity in the coefficients of an estimator.

Ridge Regression is the estimator used in this example.

Each color represents a different feature of the

coefficient vector, and this is displayed as a function of the

regularization parameter.

This example also shows the usefulness of applying Ridge regression to highly ill-conditioned matrices. For such matrices, a slight change in the target variable can cause huge variances in the calculated weights. In such cases, it is useful to set a certain regularization (alpha) to reduce this variation (noise).

When alpha is very large, the regularization effect dominates the squared loss function and the coefficients tend to zero. At the end of the path, as alpha tends toward zero and the solution tends towards the ordinary least squares, coefficients exhibit big oscillations. In practise it is necessary to tune alpha in such a way that a balance is maintained between both.

# Author: Fabian Pedregosa -- <fabian.pedregosa@inria.fr>

# License: BSD 3 clause

import matplotlib.pyplot as plt

import numpy as np

from sklearn import linear_model

# X is the 10x10 Hilbert matrix

X = 1.0 / (np.arange(1, 11) + np.arange(0, 10)[:, np.newaxis])

y = np.ones(10)

Compute paths¶

n_alphas = 200

alphas = np.logspace(-10, -2, n_alphas)

coefs = []

for a in alphas:

ridge = linear_model.Ridge(alpha=a, fit_intercept=False)

ridge.fit(X, y)

coefs.append(ridge.coef_)

Display results¶

ax = plt.gca()

ax.plot(alphas, coefs)

ax.set_xscale("log")

ax.set_xlim(ax.get_xlim()[::-1]) # reverse axis

plt.xlabel("alpha")

plt.ylabel("weights")

plt.title("Ridge coefficients as a function of the regularization")

plt.axis("tight")

plt.show()

Total running time of the script: (0 minutes 0.377 seconds)