Note

Click here to download the full example code or to run this example in your browser via Binder

Tweedie regression on insurance claims¶

This example illustrates the use of Poisson, Gamma and Tweedie regression on the French Motor Third-Party Liability Claims dataset, and is inspired by an R tutorial [1].

In this dataset, each sample corresponds to an insurance policy, i.e. a contract within an insurance company and an individual (policyholder). Available features include driver age, vehicle age, vehicle power, etc.

A few definitions: a claim is the request made by a policyholder to the insurer to compensate for a loss covered by the insurance. The claim amount is the amount of money that the insurer must pay. The exposure is the duration of the insurance coverage of a given policy, in years.

Here our goal is to predict the expected value, i.e. the mean, of the total claim amount per exposure unit also referred to as the pure premium.

There are several possibilities to do that, two of which are:

Model the number of claims with a Poisson distribution, and the average claim amount per claim, also known as severity, as a Gamma distribution and multiply the predictions of both in order to get the total claim amount.

Model the total claim amount per exposure directly, typically with a Tweedie distribution of Tweedie power \(p \in (1, 2)\).

In this example we will illustrate both approaches. We start by defining a few helper functions for loading the data and visualizing results.

# Authors: Christian Lorentzen <lorentzen.ch@gmail.com>

# Roman Yurchak <rth.yurchak@gmail.com>

# Olivier Grisel <olivier.grisel@ensta.org>

# License: BSD 3 clause

from functools import partial

import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from sklearn.datasets import fetch_openml

from sklearn.metrics import mean_tweedie_deviance

from sklearn.metrics import mean_absolute_error

from sklearn.metrics import mean_squared_error

def load_mtpl2(n_samples=100000):

"""Fetch the French Motor Third-Party Liability Claims dataset.

Parameters

----------

n_samples: int, default=100000

number of samples to select (for faster run time). Full dataset has

678013 samples.

"""

# freMTPL2freq dataset from https://www.openml.org/d/41214

df_freq = fetch_openml(data_id=41214, as_frame=True)["data"]

df_freq["IDpol"] = df_freq["IDpol"].astype(int)

df_freq.set_index("IDpol", inplace=True)

# freMTPL2sev dataset from https://www.openml.org/d/41215

df_sev = fetch_openml(data_id=41215, as_frame=True)["data"]

# sum ClaimAmount over identical IDs

df_sev = df_sev.groupby("IDpol").sum()

df = df_freq.join(df_sev, how="left")

df["ClaimAmount"].fillna(0, inplace=True)

# unquote string fields

for column_name in df.columns[df.dtypes.values == object]:

df[column_name] = df[column_name].str.strip("'")

return df.iloc[:n_samples]

def plot_obs_pred(

df,

feature,

weight,

observed,

predicted,

y_label=None,

title=None,

ax=None,

fill_legend=False,

):

"""Plot observed and predicted - aggregated per feature level.

Parameters

----------

df : DataFrame

input data

feature: str

a column name of df for the feature to be plotted

weight : str

column name of df with the values of weights or exposure

observed : str

a column name of df with the observed target

predicted : DataFrame

a dataframe, with the same index as df, with the predicted target

fill_legend : bool, default=False

whether to show fill_between legend

"""

# aggregate observed and predicted variables by feature level

df_ = df.loc[:, [feature, weight]].copy()

df_["observed"] = df[observed] * df[weight]

df_["predicted"] = predicted * df[weight]

df_ = (

df_.groupby([feature])[[weight, "observed", "predicted"]]

.sum()

.assign(observed=lambda x: x["observed"] / x[weight])

.assign(predicted=lambda x: x["predicted"] / x[weight])

)

ax = df_.loc[:, ["observed", "predicted"]].plot(style=".", ax=ax)

y_max = df_.loc[:, ["observed", "predicted"]].values.max() * 0.8

p2 = ax.fill_between(

df_.index,

0,

y_max * df_[weight] / df_[weight].values.max(),

color="g",

alpha=0.1,

)

if fill_legend:

ax.legend([p2], ["{} distribution".format(feature)])

ax.set(

ylabel=y_label if y_label is not None else None,

title=title if title is not None else "Train: Observed vs Predicted",

)

def score_estimator(

estimator,

X_train,

X_test,

df_train,

df_test,

target,

weights,

tweedie_powers=None,

):

"""Evaluate an estimator on train and test sets with different metrics"""

metrics = [

("D² explained", None), # Use default scorer if it exists

("mean abs. error", mean_absolute_error),

("mean squared error", mean_squared_error),

]

if tweedie_powers:

metrics += [

(

"mean Tweedie dev p={:.4f}".format(power),

partial(mean_tweedie_deviance, power=power),

)

for power in tweedie_powers

]

res = []

for subset_label, X, df in [

("train", X_train, df_train),

("test", X_test, df_test),

]:

y, _weights = df[target], df[weights]

for score_label, metric in metrics:

if isinstance(estimator, tuple) and len(estimator) == 2:

# Score the model consisting of the product of frequency and

# severity models.

est_freq, est_sev = estimator

y_pred = est_freq.predict(X) * est_sev.predict(X)

else:

y_pred = estimator.predict(X)

if metric is None:

if not hasattr(estimator, "score"):

continue

score = estimator.score(X, y, sample_weight=_weights)

else:

score = metric(y, y_pred, sample_weight=_weights)

res.append({"subset": subset_label, "metric": score_label, "score": score})

res = (

pd.DataFrame(res)

.set_index(["metric", "subset"])

.score.unstack(-1)

.round(4)

.loc[:, ["train", "test"]]

)

return res

Loading datasets, basic feature extraction and target definitions¶

We construct the freMTPL2 dataset by joining the freMTPL2freq table,

containing the number of claims (ClaimNb), with the freMTPL2sev table,

containing the claim amount (ClaimAmount) for the same policy ids

(IDpol).

from sklearn.pipeline import make_pipeline

from sklearn.preprocessing import FunctionTransformer, OneHotEncoder

from sklearn.preprocessing import StandardScaler, KBinsDiscretizer

from sklearn.compose import ColumnTransformer

df = load_mtpl2(n_samples=60000)

# Note: filter out claims with zero amount, as the severity model

# requires strictly positive target values.

df.loc[(df["ClaimAmount"] == 0) & (df["ClaimNb"] >= 1), "ClaimNb"] = 0

# Correct for unreasonable observations (that might be data error)

# and a few exceptionally large claim amounts

df["ClaimNb"] = df["ClaimNb"].clip(upper=4)

df["Exposure"] = df["Exposure"].clip(upper=1)

df["ClaimAmount"] = df["ClaimAmount"].clip(upper=200000)

log_scale_transformer = make_pipeline(

FunctionTransformer(func=np.log), StandardScaler()

)

column_trans = ColumnTransformer(

[

("binned_numeric", KBinsDiscretizer(n_bins=10), ["VehAge", "DrivAge"]),

(

"onehot_categorical",

OneHotEncoder(),

["VehBrand", "VehPower", "VehGas", "Region", "Area"],

),

("passthrough_numeric", "passthrough", ["BonusMalus"]),

("log_scaled_numeric", log_scale_transformer, ["Density"]),

],

remainder="drop",

)

X = column_trans.fit_transform(df)

# Insurances companies are interested in modeling the Pure Premium, that is

# the expected total claim amount per unit of exposure for each policyholder

# in their portfolio:

df["PurePremium"] = df["ClaimAmount"] / df["Exposure"]

# This can be indirectly approximated by a 2-step modeling: the product of the

# Frequency times the average claim amount per claim:

df["Frequency"] = df["ClaimNb"] / df["Exposure"]

df["AvgClaimAmount"] = df["ClaimAmount"] / np.fmax(df["ClaimNb"], 1)

with pd.option_context("display.max_columns", 15):

print(df[df.ClaimAmount > 0].head())

/home/runner/work/scikit-learn/scikit-learn/sklearn/preprocessing/_discretization.py:291: UserWarning: Bins whose width are too small (i.e., <= 1e-8) in feature 0 are removed. Consider decreasing the number of bins.

warnings.warn(

ClaimNb Exposure Area VehPower VehAge DrivAge BonusMalus VehBrand \

IDpol

139.0 1.0 0.75 F 7.0 1.0 61.0 50.0 B12

190.0 1.0 0.14 B 12.0 5.0 50.0 60.0 B12

414.0 1.0 0.14 E 4.0 0.0 36.0 85.0 B12

424.0 2.0 0.62 F 10.0 0.0 51.0 100.0 B12

463.0 1.0 0.31 A 5.0 0.0 45.0 50.0 B12

VehGas Density Region ClaimAmount PurePremium Frequency \

IDpol

139.0 Regular 27000.0 R11 303.00 404.000000 1.333333

190.0 Diesel 56.0 R25 1981.84 14156.000000 7.142857

414.0 Regular 4792.0 R11 1456.55 10403.928571 7.142857

424.0 Regular 27000.0 R11 10834.00 17474.193548 3.225806

463.0 Regular 12.0 R73 3986.67 12860.225806 3.225806

AvgClaimAmount

IDpol

139.0 303.00

190.0 1981.84

414.0 1456.55

424.0 5417.00

463.0 3986.67

Frequency model – Poisson distribution¶

The number of claims (ClaimNb) is a positive integer (0 included).

Thus, this target can be modelled by a Poisson distribution.

It is then assumed to be the number of discrete events occurring with a

constant rate in a given time interval (Exposure, in units of years).

Here we model the frequency y = ClaimNb / Exposure, which is still a

(scaled) Poisson distribution, and use Exposure as sample_weight.

from sklearn.model_selection import train_test_split

from sklearn.linear_model import PoissonRegressor

df_train, df_test, X_train, X_test = train_test_split(df, X, random_state=0)

# The parameters of the model are estimated by minimizing the Poisson deviance

# on the training set via a quasi-Newton solver: l-BFGS. Some of the features

# are collinear, we use a weak penalization to avoid numerical issues.

glm_freq = PoissonRegressor(alpha=1e-3, max_iter=400)

glm_freq.fit(X_train, df_train["Frequency"], sample_weight=df_train["Exposure"])

scores = score_estimator(

glm_freq,

X_train,

X_test,

df_train,

df_test,

target="Frequency",

weights="Exposure",

)

print("Evaluation of PoissonRegressor on target Frequency")

print(scores)

Evaluation of PoissonRegressor on target Frequency

subset train test

metric

D² explained 0.0242 0.0214

mean abs. error 0.1706 0.1660

mean squared error 0.3041 0.3043

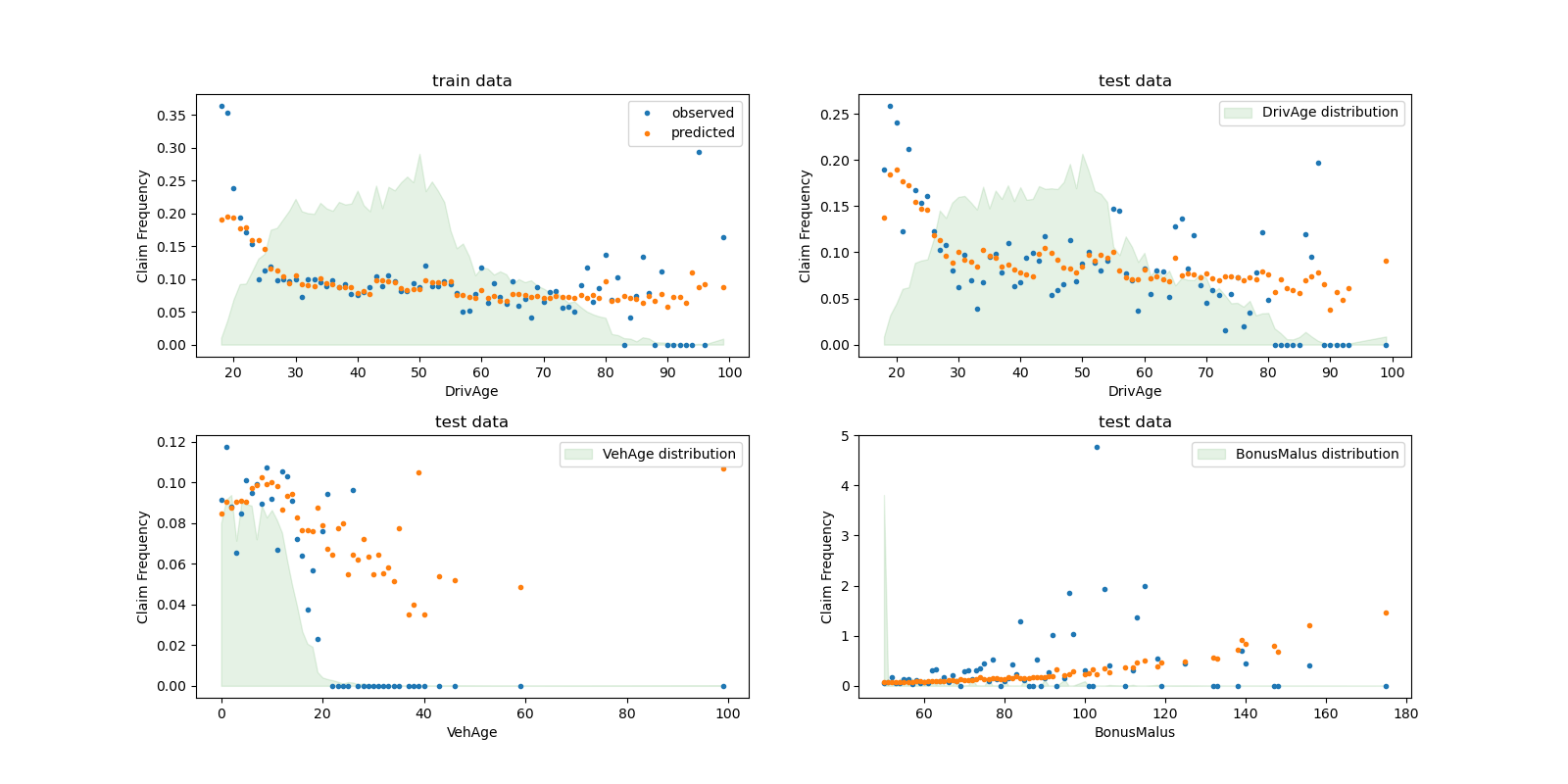

We can visually compare observed and predicted values, aggregated by the

drivers age (DrivAge), vehicle age (VehAge) and the insurance

bonus/malus (BonusMalus).

fig, ax = plt.subplots(ncols=2, nrows=2, figsize=(16, 8))

fig.subplots_adjust(hspace=0.3, wspace=0.2)

plot_obs_pred(

df=df_train,

feature="DrivAge",

weight="Exposure",

observed="Frequency",

predicted=glm_freq.predict(X_train),

y_label="Claim Frequency",

title="train data",

ax=ax[0, 0],

)

plot_obs_pred(

df=df_test,

feature="DrivAge",

weight="Exposure",

observed="Frequency",

predicted=glm_freq.predict(X_test),

y_label="Claim Frequency",

title="test data",

ax=ax[0, 1],

fill_legend=True,

)

plot_obs_pred(

df=df_test,

feature="VehAge",

weight="Exposure",

observed="Frequency",

predicted=glm_freq.predict(X_test),

y_label="Claim Frequency",

title="test data",

ax=ax[1, 0],

fill_legend=True,

)

plot_obs_pred(

df=df_test,

feature="BonusMalus",

weight="Exposure",

observed="Frequency",

predicted=glm_freq.predict(X_test),

y_label="Claim Frequency",

title="test data",

ax=ax[1, 1],

fill_legend=True,

)

According to the observed data, the frequency of accidents is higher for

drivers younger than 30 years old, and is positively correlated with the

BonusMalus variable. Our model is able to mostly correctly model this

behaviour.

Severity Model - Gamma distribution¶

The mean claim amount or severity (AvgClaimAmount) can be empirically

shown to follow approximately a Gamma distribution. We fit a GLM model for

the severity with the same features as the frequency model.

Note:

We filter out

ClaimAmount == 0as the Gamma distribution has support on \((0, \infty)\), not \([0, \infty)\).We use

ClaimNbassample_weightto account for policies that contain more than one claim.

from sklearn.linear_model import GammaRegressor

mask_train = df_train["ClaimAmount"] > 0

mask_test = df_test["ClaimAmount"] > 0

glm_sev = GammaRegressor(alpha=10.0, max_iter=10000)

glm_sev.fit(

X_train[mask_train.values],

df_train.loc[mask_train, "AvgClaimAmount"],

sample_weight=df_train.loc[mask_train, "ClaimNb"],

)

scores = score_estimator(

glm_sev,

X_train[mask_train.values],

X_test[mask_test.values],

df_train[mask_train],

df_test[mask_test],

target="AvgClaimAmount",

weights="ClaimNb",

)

print("Evaluation of GammaRegressor on target AvgClaimAmount")

print(scores)

Evaluation of GammaRegressor on target AvgClaimAmount

subset train test

metric

D² explained 3.000000e-03 -9.600000e-03

mean abs. error 1.699197e+03 2.027923e+03

mean squared error 4.548147e+07 6.094863e+07

Here, the scores for the test data call for caution as they are significantly worse than for the training data indicating an overfit despite the strong regularization.

Note that the resulting model is the average claim amount per claim. As such, it is conditional on having at least one claim, and cannot be used to predict the average claim amount per policy in general.

print(

"Mean AvgClaim Amount per policy: %.2f "

% df_train["AvgClaimAmount"].mean()

)

print(

"Mean AvgClaim Amount | NbClaim > 0: %.2f"

% df_train["AvgClaimAmount"][df_train["AvgClaimAmount"] > 0].mean()

)

print(

"Predicted Mean AvgClaim Amount | NbClaim > 0: %.2f"

% glm_sev.predict(X_train).mean()

)

Mean AvgClaim Amount per policy: 97.89

Mean AvgClaim Amount | NbClaim > 0: 1899.60

Predicted Mean AvgClaim Amount | NbClaim > 0: 1884.40

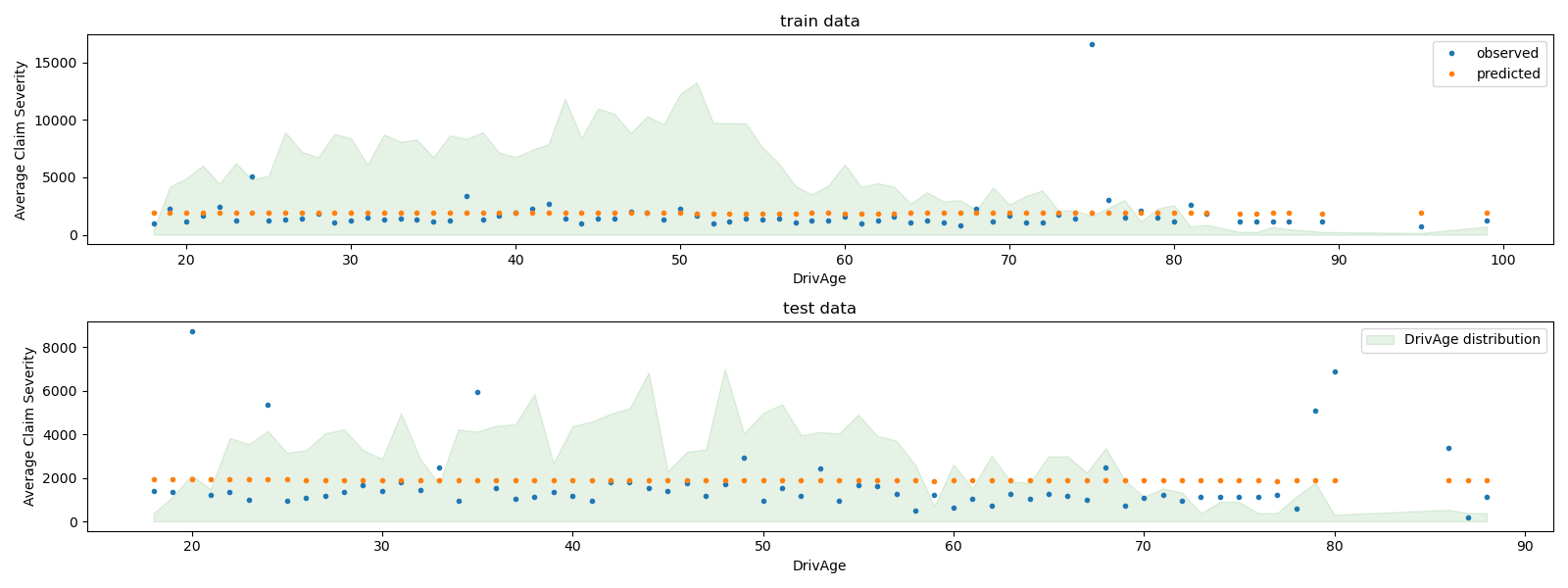

We can visually compare observed and predicted values, aggregated for

the drivers age (DrivAge).

fig, ax = plt.subplots(ncols=1, nrows=2, figsize=(16, 6))

plot_obs_pred(

df=df_train.loc[mask_train],

feature="DrivAge",

weight="Exposure",

observed="AvgClaimAmount",

predicted=glm_sev.predict(X_train[mask_train.values]),

y_label="Average Claim Severity",

title="train data",

ax=ax[0],

)

plot_obs_pred(

df=df_test.loc[mask_test],

feature="DrivAge",

weight="Exposure",

observed="AvgClaimAmount",

predicted=glm_sev.predict(X_test[mask_test.values]),

y_label="Average Claim Severity",

title="test data",

ax=ax[1],

fill_legend=True,

)

plt.tight_layout()

Overall, the drivers age (DrivAge) has a weak impact on the claim

severity, both in observed and predicted data.

Pure Premium Modeling via a Product Model vs single TweedieRegressor¶

As mentioned in the introduction, the total claim amount per unit of exposure can be modeled as the product of the prediction of the frequency model by the prediction of the severity model.

Alternatively, one can directly model the total loss with a unique

Compound Poisson Gamma generalized linear model (with a log link function).

This model is a special case of the Tweedie GLM with a “power” parameter

\(p \in (1, 2)\). Here, we fix apriori the power parameter of the

Tweedie model to some arbitrary value (1.9) in the valid range. Ideally one

would select this value via grid-search by minimizing the negative

log-likelihood of the Tweedie model, but unfortunately the current

implementation does not allow for this (yet).

We will compare the performance of both approaches.

To quantify the performance of both models, one can compute

the mean deviance of the train and test data assuming a Compound

Poisson-Gamma distribution of the total claim amount. This is equivalent to

a Tweedie distribution with a power parameter between 1 and 2.

The sklearn.metrics.mean_tweedie_deviance depends on a power

parameter. As we do not know the true value of the power parameter, we here

compute the mean deviances for a grid of possible values, and compare the

models side by side, i.e. we compare them at identical values of power.

Ideally, we hope that one model will be consistently better than the other,

regardless of power.

from sklearn.linear_model import TweedieRegressor

glm_pure_premium = TweedieRegressor(power=1.9, alpha=0.1, max_iter=10000)

glm_pure_premium.fit(

X_train, df_train["PurePremium"], sample_weight=df_train["Exposure"]

)

tweedie_powers = [1.5, 1.7, 1.8, 1.9, 1.99, 1.999, 1.9999]

scores_product_model = score_estimator(

(glm_freq, glm_sev),

X_train,

X_test,

df_train,

df_test,

target="PurePremium",

weights="Exposure",

tweedie_powers=tweedie_powers,

)

scores_glm_pure_premium = score_estimator(

glm_pure_premium,

X_train,

X_test,

df_train,

df_test,

target="PurePremium",

weights="Exposure",

tweedie_powers=tweedie_powers,

)

scores = pd.concat(

[scores_product_model, scores_glm_pure_premium],

axis=1,

sort=True,

keys=("Product Model", "TweedieRegressor"),

)

print("Evaluation of the Product Model and the Tweedie Regressor on target PurePremium")

with pd.option_context("display.expand_frame_repr", False):

print(scores)

Evaluation of the Product Model and the Tweedie Regressor on target PurePremium

Product Model TweedieRegressor

subset train test train test

metric

D² explained NaN NaN 2.650000e-02 2.580000e-02

mean Tweedie dev p=1.5000 8.216730e+01 8.640090e+01 7.960780e+01 8.618690e+01

mean Tweedie dev p=1.7000 3.833270e+01 3.920430e+01 3.737380e+01 3.917450e+01

mean Tweedie dev p=1.8000 3.106620e+01 3.148760e+01 3.047890e+01 3.148130e+01

mean Tweedie dev p=1.9000 3.396070e+01 3.420620e+01 3.360060e+01 3.420820e+01

mean Tweedie dev p=1.9900 1.989231e+02 1.996421e+02 1.986911e+02 1.996461e+02

mean Tweedie dev p=1.9990 1.886428e+03 1.892749e+03 1.886206e+03 1.892753e+03

mean Tweedie dev p=1.9999 1.876452e+04 1.882692e+04 1.876430e+04 1.882692e+04

mean abs. error 3.245679e+02 3.468485e+02 3.202459e+02 3.397022e+02

mean squared error 1.469185e+08 3.325898e+07 1.469327e+08 3.325470e+07

In this example, both modeling approaches yield comparable performance metrics. For implementation reasons, the percentage of explained variance \(D^2\) is not available for the product model.

We can additionally validate these models by comparing observed and predicted total claim amount over the test and train subsets. We see that, on average, both model tend to underestimate the total claim (but this behavior depends on the amount of regularization).

res = []

for subset_label, X, df in [

("train", X_train, df_train),

("test", X_test, df_test),

]:

exposure = df["Exposure"].values

res.append(

{

"subset": subset_label,

"observed": df["ClaimAmount"].values.sum(),

"predicted, frequency*severity model": np.sum(

exposure * glm_freq.predict(X) * glm_sev.predict(X)

),

"predicted, tweedie, power=%.2f"

% glm_pure_premium.power: np.sum(exposure * glm_pure_premium.predict(X)),

}

)

print(pd.DataFrame(res).set_index("subset").T)

subset train test

observed 4.577616e+06 1.725665e+06

predicted, frequency*severity model 4.562939e+06 1.494451e+06

predicted, tweedie, power=1.90 4.451558e+06 1.431963e+06

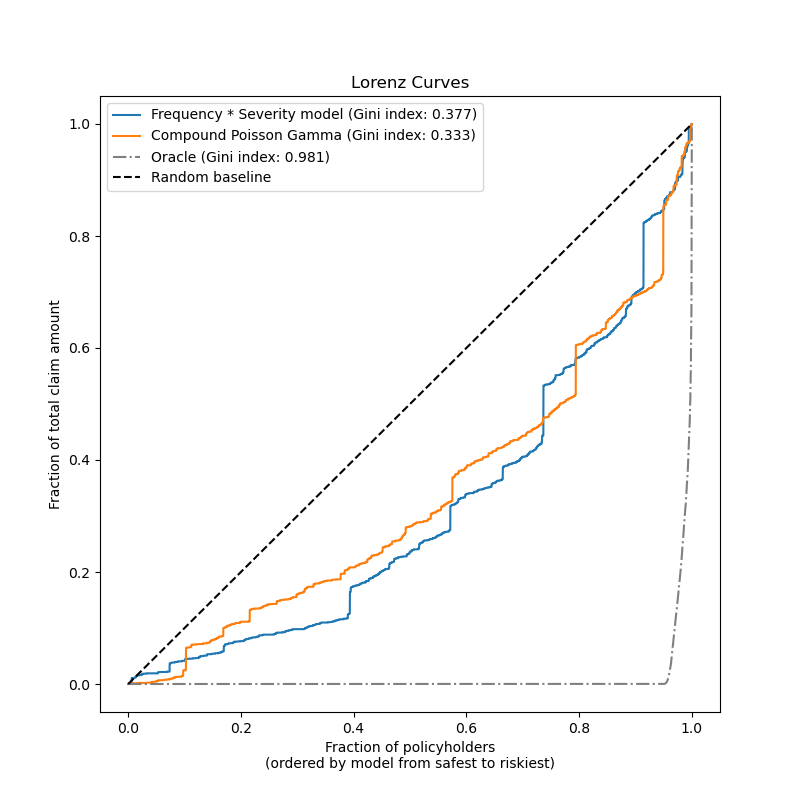

Finally, we can compare the two models using a plot of cumulated claims: for each model, the policyholders are ranked from safest to riskiest based on the model predictions and the fraction of observed total cumulated claims is plotted on the y axis. This plot is often called the ordered Lorenz curve of the model.

The Gini coefficient (based on the area between the curve and the diagonal) can be used as a model selection metric to quantify the ability of the model to rank policyholders. Note that this metric does not reflect the ability of the models to make accurate predictions in terms of absolute value of total claim amounts but only in terms of relative amounts as a ranking metric. The Gini coefficient is upper bounded by 1.0 but even an oracle model that ranks the policyholders by the observed claim amounts cannot reach a score of 1.0.

We observe that both models are able to rank policyholders by risky-ness significantly better than chance although they are also both far from the oracle model due to the natural difficulty of the prediction problem from a few features: most accidents are not predictable and can be caused by environmental circumstances that are not described at all by the input features of the models.

Note that the Gini index only characterizes the ranking performance of the model but not its calibration: any monotonic transformation of the predictions leaves the Gini index of the model unchanged.

Finally one should highlight that the Compound Poisson Gamma model that is directly fit on the pure premium is operationally simpler to develop and maintain as it consists of a single scikit-learn estimator instead of a pair of models, each with its own set of hyperparameters.

from sklearn.metrics import auc

def lorenz_curve(y_true, y_pred, exposure):

y_true, y_pred = np.asarray(y_true), np.asarray(y_pred)

exposure = np.asarray(exposure)

# order samples by increasing predicted risk:

ranking = np.argsort(y_pred)

ranked_exposure = exposure[ranking]

ranked_pure_premium = y_true[ranking]

cumulated_claim_amount = np.cumsum(ranked_pure_premium * ranked_exposure)

cumulated_claim_amount /= cumulated_claim_amount[-1]

cumulated_samples = np.linspace(0, 1, len(cumulated_claim_amount))

return cumulated_samples, cumulated_claim_amount

fig, ax = plt.subplots(figsize=(8, 8))

y_pred_product = glm_freq.predict(X_test) * glm_sev.predict(X_test)

y_pred_total = glm_pure_premium.predict(X_test)

for label, y_pred in [

("Frequency * Severity model", y_pred_product),

("Compound Poisson Gamma", y_pred_total),

]:

ordered_samples, cum_claims = lorenz_curve(

df_test["PurePremium"], y_pred, df_test["Exposure"]

)

gini = 1 - 2 * auc(ordered_samples, cum_claims)

label += " (Gini index: {:.3f})".format(gini)

ax.plot(ordered_samples, cum_claims, linestyle="-", label=label)

# Oracle model: y_pred == y_test

ordered_samples, cum_claims = lorenz_curve(

df_test["PurePremium"], df_test["PurePremium"], df_test["Exposure"]

)

gini = 1 - 2 * auc(ordered_samples, cum_claims)

label = "Oracle (Gini index: {:.3f})".format(gini)

ax.plot(ordered_samples, cum_claims, linestyle="-.", color="gray", label=label)

# Random baseline

ax.plot([0, 1], [0, 1], linestyle="--", color="black", label="Random baseline")

ax.set(

title="Lorenz Curves",

xlabel="Fraction of policyholders\n(ordered by model from safest to riskiest)",

ylabel="Fraction of total claim amount",

)

ax.legend(loc="upper left")

plt.plot()

[]

Total running time of the script: ( 0 minutes 20.779 seconds)